Figures & data

Table 1. Sample Descriptive Statistics by Sector and Market Type.

Panel A. Beginning of Time Period (2004Q1)

Panel B. End of Time Period (2019Q4)

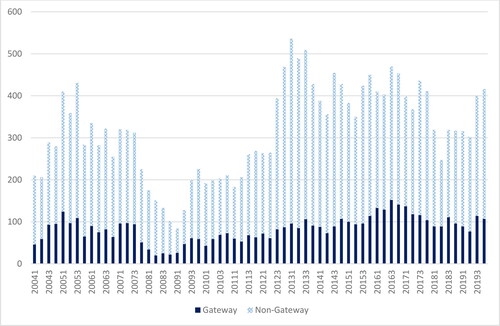

Figure 1. Cumulative number of sales. Note: The figure displays the three-quarter (centered) cumulative number of true sales in the cleaned dataset.

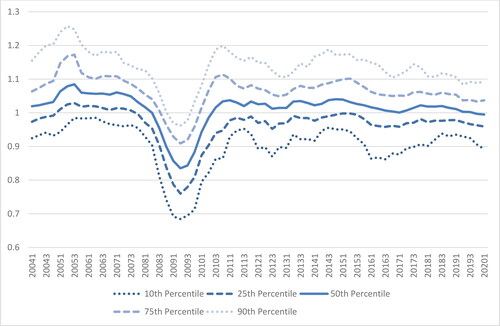

Figure 2. Ratios of sale prices to appraised values. Note: The figure depicts the median (50th percentile) of the three-quarter average of the ratio of sale price to the lagged appraised value as well as the 10th, 25th, 75th, and 90th percentiles.

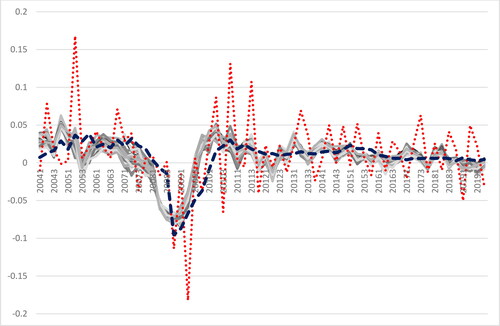

Figure 3. Portfolio and market appreciation returns. Note: The solid lines are the returns of 30 randomly selected portfolios, the dashed line is the NCREIF Property Index (NPI), and the dotted line the value-weighted NCREIF Transaction-Based Index (NTBI).

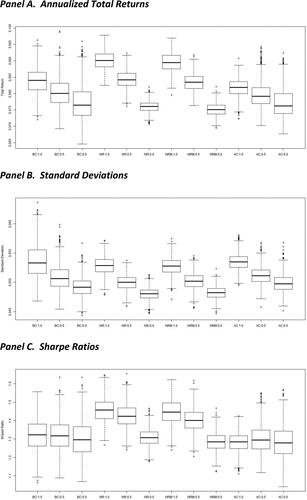

Figure 4. Distributions of portfolio total returns, standard deviations, and Sharpe ratios. Note: BC = base case, NR = quality control using NOI ratios, NRM = quality control using NOI ratios by market class, and AC = age-corrected quality control. 1.0, 0.5, and 0.0 indicate the allocation to gateway markets (100%, 50%, and 0%, respectively).

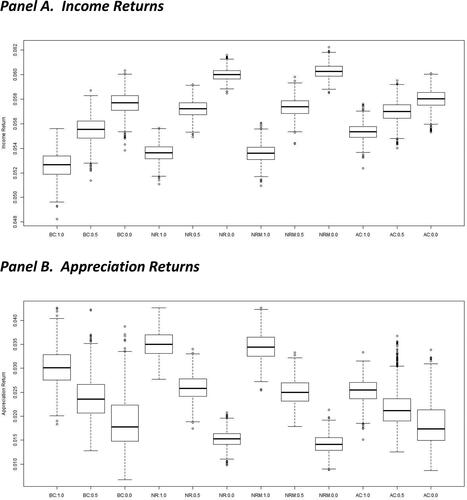

Figure 5. Distributions of annualized portfolio income and appreciation returns. Note: BC = base case, NR = quality control using NOI ratios, NRM = quality control using NOI ratios by market class, and AC = age-corrected quality control. 1.0, 0.5, and 0.0 indicate the allocation to gateway markets (100%, 50%, and 0%, respectively).

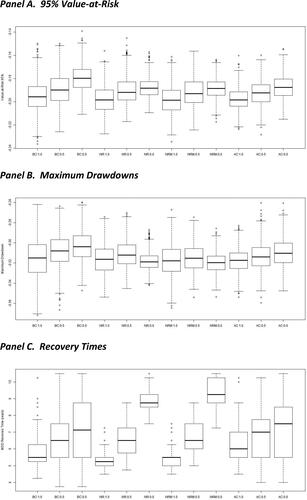

Figure 6. Portfolio downside risk measures. Note: BC = base case, NR = quality control using NOI ratios, NRM = quality control using NOI ratios by market class, and AC = age-corrected quality control. 1.0, 0.5, and 0.0 indicate the allocation to gateway markets (100%, 50%, and 0%, respectively).

Table 2. Selected Performance Metrics for Various Sets of Gateway Markets.

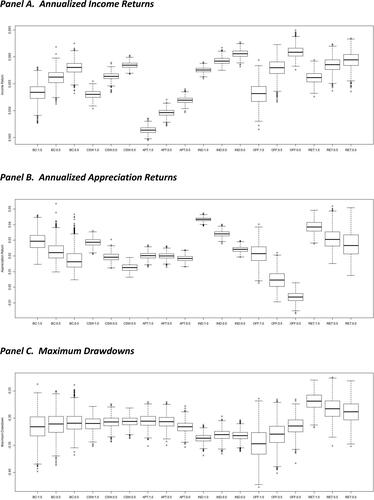

Figure 7. Robustness checks for sectoral composition and sectors. Note: BC = base case, CSW = constant sector weights, APT = apartments, IND = industrial, OFF = office, and RET = retail. 1.0, 0.5, and 0.0 indicate the allocation to gateway markets (100%, 50%, and 0%, respectively).

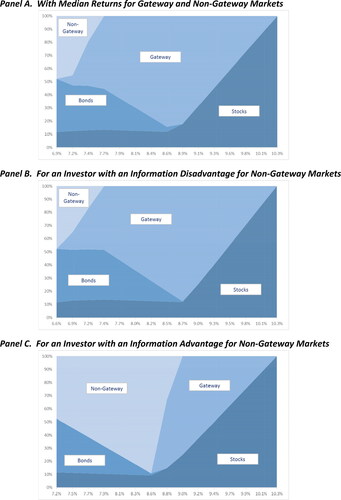

Figure 8. Composition of mixed-asset portfolios.

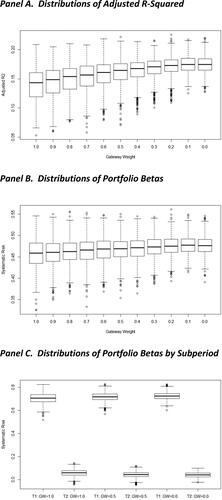

Figure 9. Distributions of adjusted R-squared and portfolio betas. Note: T1 = 2004Q1–2011Q4 and T2 = 2012Q1–2019Q4.

Panel A. Six Gateway Markets

Panel B. Additional Markets