Figures & data

Table 1. Sample selection and distribution of observations across years

Table 2. Descriptive statistics

Table 3. Panel regressions for cost of equity capital on overall disclosure

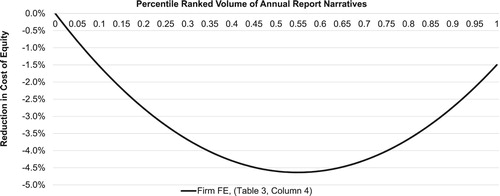

Figure 1. U-shaped relation between cost of equity capital and volume of annual report narratives. This figure illustrates the reduction in the cost of equity capital as a function of the (ranked) volume of annual report narratives, as implied by the regression results in Table , column (4) (that is after allowing for firm fixed effects)

Table 4. Three-year rolling window regressions showing variation over time in optimum levels of disclosure

Table 5. Firm learning effects and disclosure adjustments

Table 6. Regulatory change and clutter

Table 7. Individual component analysis

Supplemental material