Figures & data

Table 1. Interviews with individuals involved in Siemens’ annual report restructuring

Table 2. Articles and conference presentations by Siemens personnel

Table 3. Siemens’ annual reports from 1998 to 2020

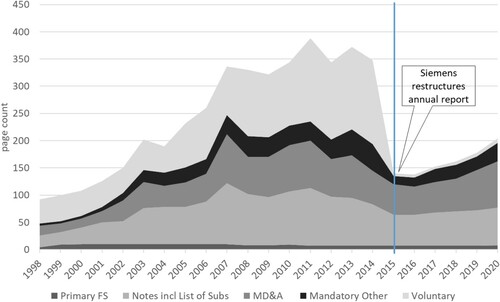

Figure 1. Development of Siemens’ annual report length over time (1998–2020).

Note: visualizes the information in Table 3, which reports the page counts of the different main sections within Siemens’ annual reports for the years 1998 through 2020. We distinguish between five elements: (1) the primary financial statements (income statement, statement of comprehensive income, balance sheet, statement of changes in shareholders’ equity, and statement of cash flows); (2) the notes to the financial statements including, when contained in the annual report, the mandatory list of subsidiaries; (3) the combined management report (excluding the voluntary sustainability and strategy sections); (4) mandatory other information; and (5) voluntary information. The vertical line demarcates the beginning of 2015, the year of Siemens’ first annual report after the annual report restructuring. Section 4.1 describes the underlying reporting requirements in more detail, and also explains Siemens’ distinction between the voluntary ‘Book 1’ of the annual report, and the largely mandatory ‘Book 2.’

Table 4. Media articles authored by parties external to Siemens

Table 5. Interviews with peer firms’ Chief Accounting Officers (CAOs)