Figures & data

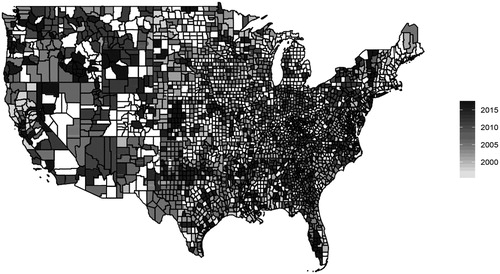

Figure 1. Map of counties selected for the study.

Note. This map shows the counties selected for our study. These are the counties that experienced a major flood disaster but were not affected by a similar disaster in the preceding three years and the following two years. Darker shades represent more recent disaster declarations, and lighter shades represent older disasters. Only the most recent disaster is included for counties that appear more than once in the sample.

Table 1. Summary statistics: Mortgage applications sample.

Table 2. Summary statistics: Mortgage performance sample.

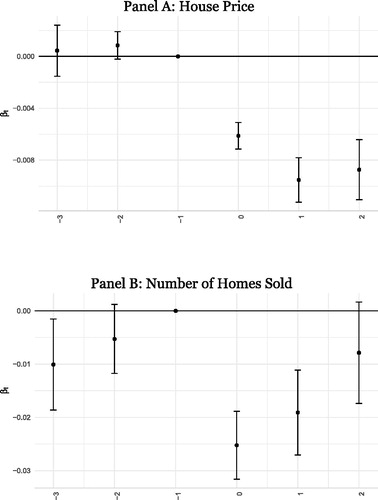

Figure 2. Impact of flood disasters on house prices and market activity.

Note. This figure presents the estimation results of regressions aimed at understanding the changes to house prices and the number of homes sold in a ZIP code after a flood disaster. The y -axis plots the estimated βt and the corresponding confidence intervals of the following specification. t represents dummy variables that indicate the number of years since the flood disaster in ZIP code g. The dependent variables in Panel A and Panel B are log(house price) and log(number of homes sold) respectively. μg and μy are ZIP code and calendar year fixed effects, respectively.

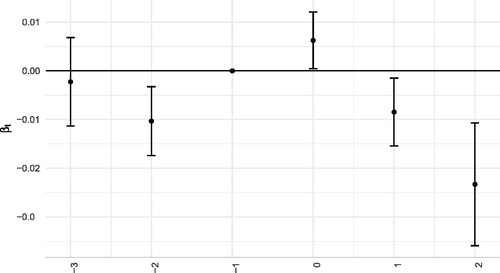

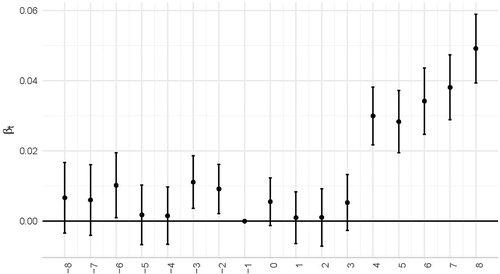

Figure 3. Mortgage applicants’ income after flood disasters (staggered DiD).

Note. This figure presents the estimation results of regressions aimed at understanding the changes to mortgage applicants’ income after a flood disaster. The y -axis plots the estimated βt and the corresponding confidence intervals of the following specification. t represents dummy variables that indicate the number of years since the flood disaster in census tract g. The dependent variables is log(mortgage applicant’s income) and μg and μy are census tract and calendar year fixed effects respectively. The sample consists of successful mortgage applications to purchase owner-occupied homes.

Table 3. Mortgage applicants’ income after flood disasters (staggered DiD).

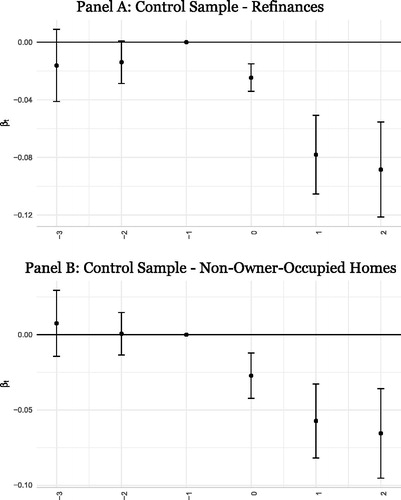

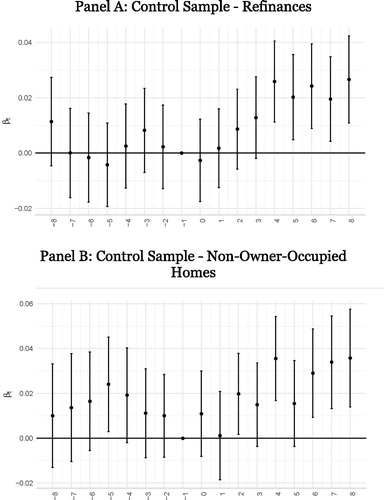

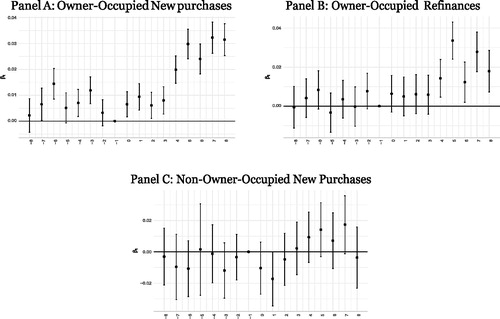

Figure 4. Changes in new home purchasers’ income relative to the control groups.

Note. This figure presents estimation results of regressions aimed at understanding the changes to the income of mortgage applicants who are purchasing new homes relative to mortgage applicants who are just refinancing and relative to mortgage applicants who are purchasing non-owner-occupied homes. The y -axis plots the estimated βt and the corresponding confidence intervals of the following specification. t represents dummy variables that indicate the number of years since the flood disaster in census tract g.

Table 4. Mortgage applicants’ income after flood disasters (generalized DiD).

Table 5. Mortgage applicants’ income after repeated flood disasters.

Figure 5. Mortgage delinquency rates (staggered DiD).

Note. This figure presents the estimation results of regressions aimed at understanding the difference in the likelihood of mortgage borrowers to become seriously delinquent, depending on whether the mortgage was originated before or after the disaster. The y -axis plots the estimated βt and the corresponding confidence intervals of the following specification. t represents dummy variables that indicate the number of quarters since the flood disaster in ZIP code g. The dependent variable is a dummy variable that indicates whether the mortgage became 150 days or more delinquent at some point after origination. μg and μy are ZIP code and calendar quarter fixed effects, respectively.

Table 6. Mortgage delinquency rates (staggered DiD).

Figure 6. Differences in delinquency rates compared to control groups.

Note. This figure presents estimation results of regressions aimed at understanding the differences in the probability of default of mortgages that finance new purchases of owner-occupied homes relative to mortgages that refinance existing mortgages or mortgages that finance the purchases of non-owner-occupied homes. The y -axis plots the estimated βt and the corresponding confidence intervals of the following specification. t represents dummy variables that indicate the number of quarters since the flood disaster in ZIP code g. The dependent variable is a dummy variable that indicates whether the mortgage became 150 days or more delinquent at some point after origination. μgy are census tract calendar year fixed effects. Controls samples in Panel A and Panel B refinance mortgages and non-owner-occupied home purchase mortgages, respectively.

Table 7. Mortgage delinquency rates (generalized DiD).

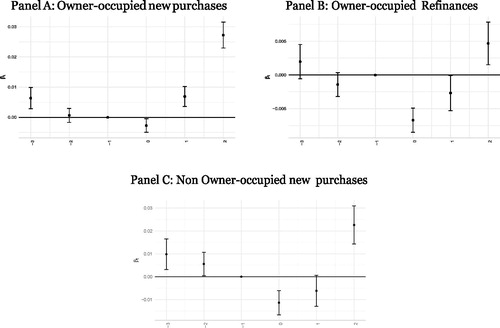

Figure 7. Mortgage interest rates (staggered DiD).

Note. This figure presents the estimation results of regressions aimed at understanding the changes to interest rates charged by mortgage lenders after a flood disaster. The y -axis plots the estimated βt and the corresponding confidence intervals of the following specification. t represents dummy variables that indicate the number of quarters since the flood disaster in ZIP code g. The dependent variables is log(interest rate) and μg and μy are ZIP code and calendar quarter fixed effects respectively. Samples in Panels A, B, and C consist of mortgages used to finance new purchases of owner-occupied homes, refinance existing mortgages backed by owner-occupied homes, and new purchases of non-owner-occupied homes, respectively.

Figure 8. Likelihood to securitize (staggered DiD).

Note. This figure presents the estimation results of regressions aimed at understanding the changes to the probability of securitizing mortgages originated after a flood disaster. The y -axis plots the estimated βt and the corresponding confidence intervals of the following specification. t represents dummy variables that indicate the number of years since the flood disaster in census tract g. The dependent variable is a dummy variable that indicates whether a particular mortgage i was securitized and μg and μy are census tract and calendar year fixed effects, respectively. Samples in Panels A, B, and C consist of mortgages used to finance new purchases of owner-occupied homes, refinance existing mortgages backed by owner-occupied homes, and new purchases of non-owner-occupied homes respectively.