Figures & data

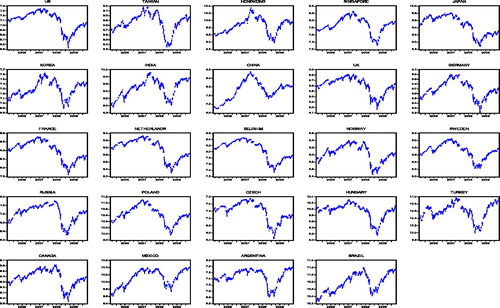

Figure 1. Logarithms of the stock indices in 24 stock markets. Source:

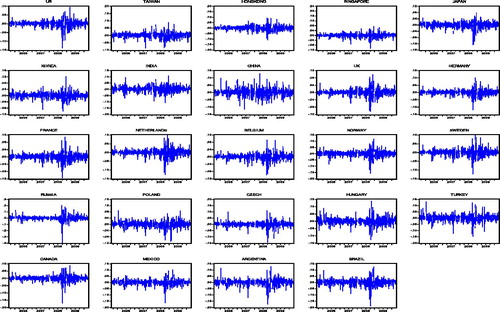

Figure 2. The stock index returns in 24 stock markets. Source:

Table 1. Summary statistics for returns on stock indices.

Table 2. Results of various unit root tests.

Table 3. Results of the non-linear unit root test – the KSS test.

Table 4. ARMA (p, q)-GARCH (1, 1) modeling and results of the ARCH-LM test for the volatility of returns.

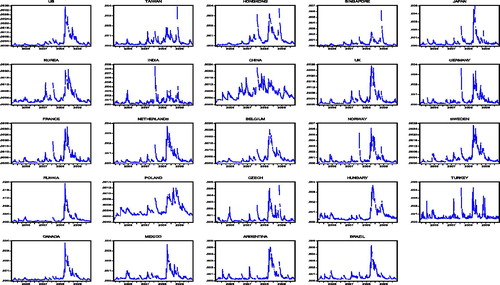

Figure 3. The volatility of returns in 24 stock markets. Source:

Table 5. Results of non-conditional correlation coefficients of returns.

Table 6. Results of correlation coefficients of volatility of returns.

Table 7. Results of the Engle-Granger test for co-integration.

Table 8. Results of the Enders-Siklos test for threshold co-integration.

Table 9. Results of the logistic smooth transition co-integration test.