Figures & data

Table 1. Geographical coverage of the research sample.

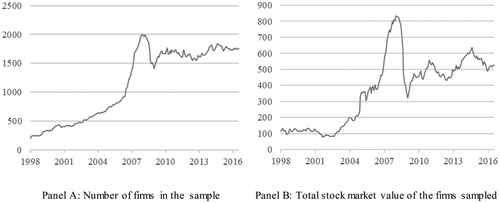

Figure 1. The research sample. Note. The figure presents the changes in the research sample over time.

Table 2. Performance of equity meta-anomalies.

Table 3. Performance of meta-anomalies under both regimes.

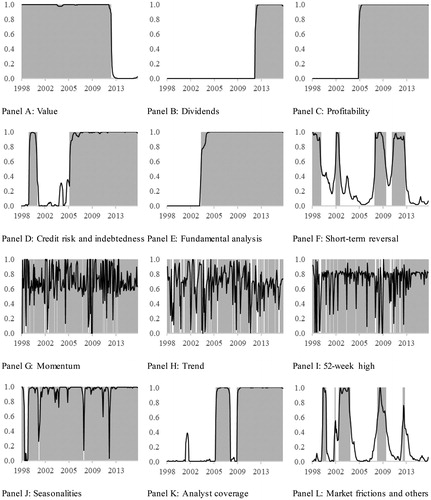

Figure 2. Time series probabilities of remaining in a regime that results in significant positive returns. Note: This figure presents the probabilities of remaining in a regime that yields significant positive returns on meta-anomalies. Shaded areas represent the periods during which probability exceeds 0.5.

Table 4. Performance of portfolios of meta-anomalies formed using Markov switching model predictions.

Table 5. Monthly returns on alternative portfolios of meta-anomalies formed using Markov switching model predictions.