Figures & data

Table 1. Spending multipliers: baseline model with k = 1 lag.

Table 2. Spending multipliers: baseline model with k = 4 lags.

Table 3. Peak spending multipliers for Poland; specifications without the ‘crisis’ dummy variable.

Table A1. Unit root test for variables (data in log).

Table A2. Lag length criteria for the baseline model.

Table A3. Elements of A and B matrices for the baseline model.

Table A4. Elements of A and B matrices – model with direct taxes, k = 1 lag.

Table A5. Elements of A and B matrices – model with direct taxes, k = 4 lags.

Table A6. Elements of A and B matrices – model with indirect taxes, k = 1 lag.

Table A7. Elements of A and B matrices – model with indirect taxes, k = 4 lags.

Table A8. Elements of A and B matrices – the baseline model with 4 lags.

Table A9. Elements of A and B matrices – subsample since 2007.

Table A10. Peak multipliers (adjusted to be interpreted in the national currency) in robust system specifications.

Table A11. Elements of A and B matrices, the additional SVAR specification for Poland.

Figure A1. Inverse roots of AR Characteristic Polynomial for baseline model.

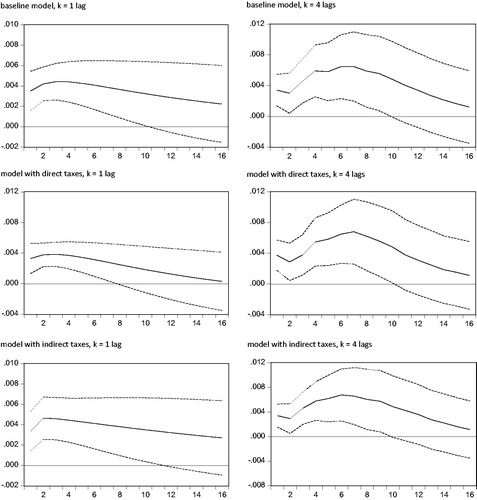

Figure A2. Impulse responses of Y to structural one s.d. shock in G ± 2 s.e., baseline model.

Figure A3. Impulse responses of Y to structural one s.d. shock in G ± 2 s.e., model with direct taxes, k = 1 lag.

Figure A4. Impulse responses of Y to structural one s.d. shock in G ± 2 s.e., model with direct taxes, k = 4 lags.

Figure A5. Impulse responses of Y to structural one s.d. shock in G ± 2 s.e., model with indirect taxes, k = 1 lag.

Figure A6. Impulse responses of Y to structural one s.d. shock in G ± 2 s.e., model with indirect taxes, k = 4 lags.

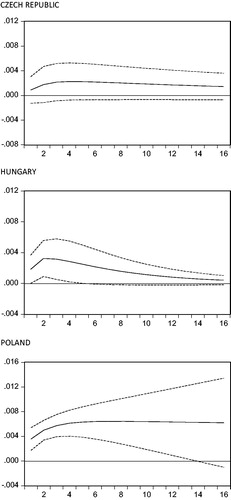

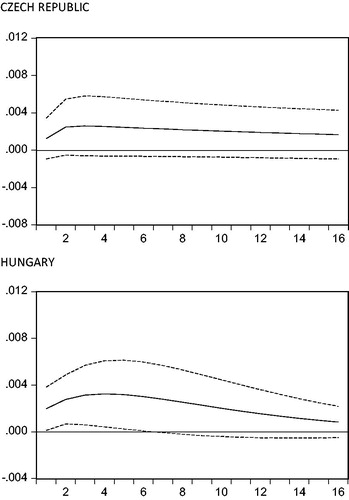

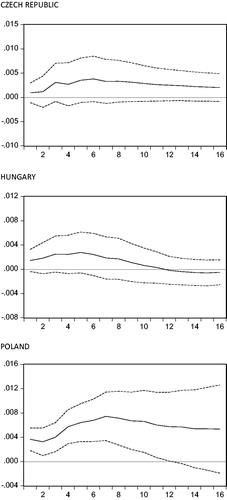

Figure A7. Impulse responses of Y to structural one s.d. shock in G ± 2 s.e., baseline SVAR with k = 4 lags.

Figure A8. Impulse responses of Y to structural one s.d. shock in G ± 2 s.e., subsample since 2007.

Figure A9. Impulse responses of Y to structural one s.d. shock in G ± 2 s.e. for Poland, SVAR specifications without the dummy variable for the crisis and post-crisis period.