Figures & data

Table 1. Results of intermittent regression estimation.

Table 2. Results of Wright and Blaire-Contreras variance ratio test.

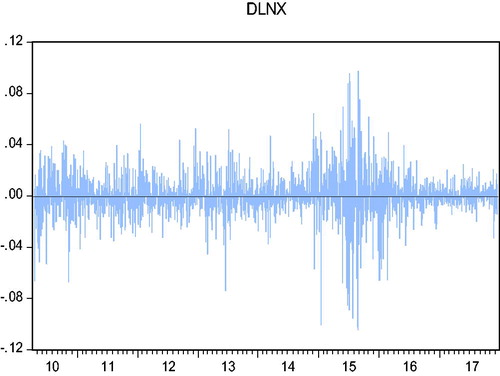

Figure 1. Daily yield of CSI 300 futures.

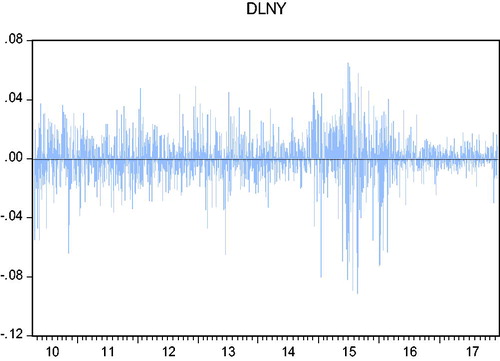

Figure 2. Daily return of CSI 300.

Table 3. ARCH effect test of and

sequences of ECM model.

Table 4. Dynamic hedging ratio and effectiveness.

Table 5. Results of linear and nonlinear Granger test.