Figures & data

Table 1. Overview of the selected previous studies which analyse financial integration in CEE and SEE.

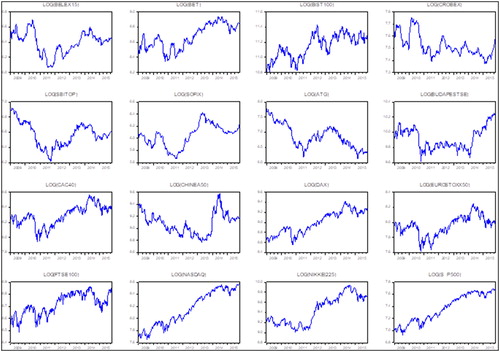

Figure 1. Stock indices during the year 2009 and 2015.

Source: DataStream.

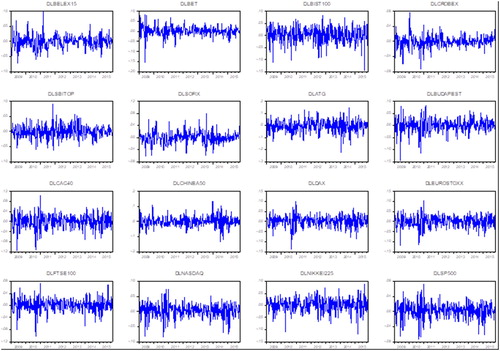

Figure 2. Returns of stock prices indices.

Source: DataStream, returns on stocks are calculated by authors.

Table 2. Descriptive statistics of stock returns.

Table 3. Unconditional correlations.

Table 4. The results of returns and volatility spillover tests-Serbia.

Table 5. The results of return and volatility spillover tests-Romania.

Table 6. The results of return and volatility spillover tests-Turkey.

Table 7. The results of return and volatility spillover tests-Croatia.

Table 8. The results of return and volatility spillover tests-Slovenia.

Table 9. The results of return and volatility spillover tests-Bulgaria.