Figures & data

Table 1. Descriptive statistics for the returns of exchange rates in major exchange markets.

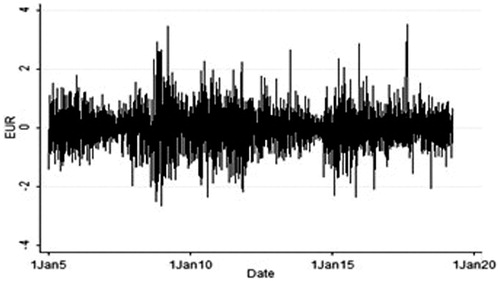

Figure 1. The daily return series of EUR. Source: Author calculations.

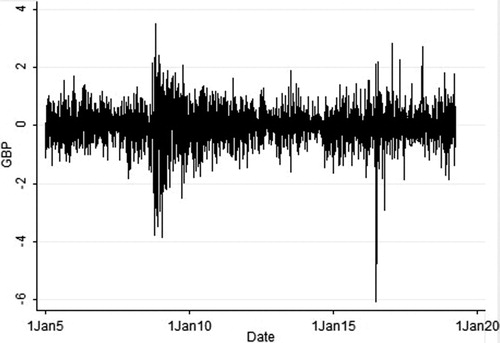

Figure 2. The daily return series of GBP. Source: Author calculations.

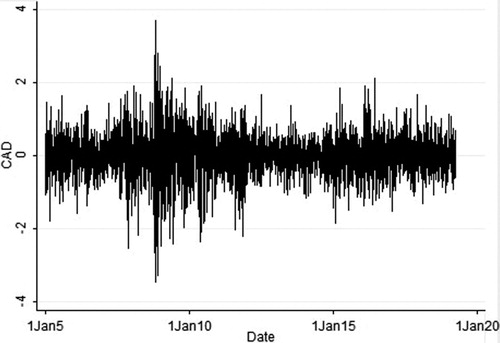

Figure 3. The daily return series of CAD. Source: Author calculations.

Figure 4. The daily return series of JPY. Source: Author calculations.

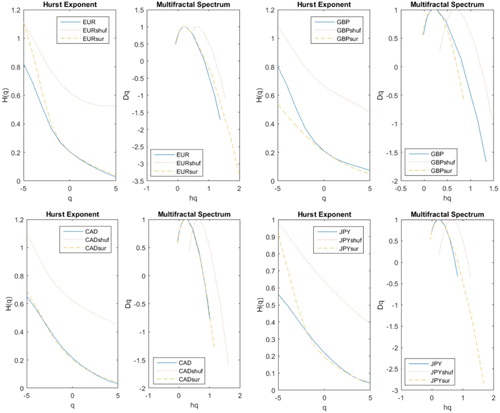

Figure 5. The Hurst exponent and multifractal spectrum of the daily returns of four exchange rates. (Notes: describes the Hurst exponent and multifractal spectrum of EUR, GBP, CAD and JPY, respectively. H(q), hq and Dq denote order value, q-order Hurst exponent, singularity strength and singularity spectrum, respectively.). Source: Author calculations.

Table 2. Multifractal properties of four exchange rate returns.

Table 3. MD values of four exchange rate returns in different periods.

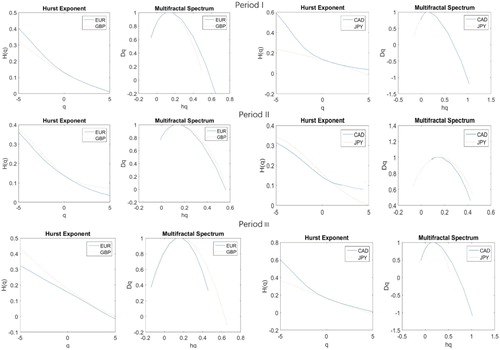

Figure 6. The Hurst Exponent and Multifractal Spectrum of exchange rate return series during Period I, II, III. Source: Author calculations.