Figures & data

Table 1. Panel unit root test.

Table 2. Autoregressive distributed lag (ARDL) test.

Table 3. Robustness test.

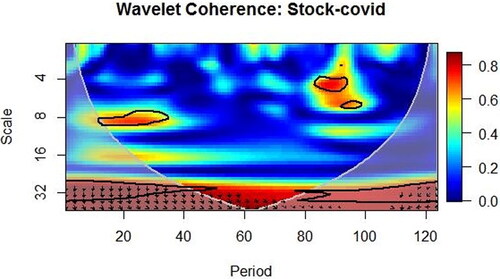

Figure 1. Wavelet coherence between stock return and COVID-19 cases.

Source: Authors calculation.

Table 4. Effects of Covid-19 on stock market volatility.

Table 5. Unit root test.

Table 6. AR (1) – GJR (1, 1) model estimates1.

Table 7. GARCHX estimation for robustness for GFI and SMVI co-movement.