Figures & data

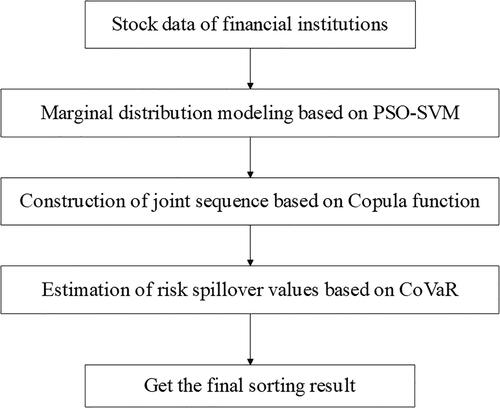

Figure 1. The flow chart of PSO-SVM-Copula-CoVaR model.

Source: Authors.

Table 1. Basic information of financial institutions.

Table 3. CoVaR results of different marginal distribution estimation methods (calculation results based on Shanghai Securities Composite Index).

Table 2. Mean square error of different marginal distribution methods.

Table 4. CoVaR results of different marginal distribution estimation methods (calculation results based on Shenzhen Securities Component Index).

Table A1. Six different copula functions.

Table A2. Descriptive statistics of financial institutions’ yield series.