Figures & data

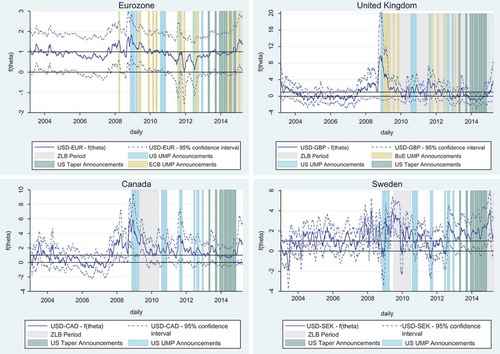

Figure 1. Foreign exchange rates sensitivity to news.

Notes: 52-business day (2 months) moving average of the fitted values of Equation 3. The foreign uncertainty variable included in the regression on the British pound is the Eurozone uncertainty variable because domestic and US uncertainty were highly correlated, and the EMU uncertainty variable can capture some relevant ‘international’ volatility. The highlighted policy announcement dates capture a 22-business day window. is set to an average value of one during the benchmark sample, which includes the period where domestic policy rates are at or above 2%.

Supplemental material