Figures & data

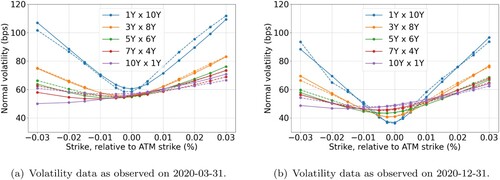

Figure 1. EUR 6M implied volatilities of co-terminal swaptions (solid) and Cheyette model calibration results (dashed) as a function of the strike, for different expiries and tenors. (a) Volatility data as observed on 2020-03-31 and (b) Volatility data as observed on 2020-12-31.

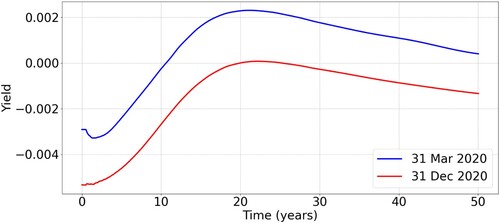

Figure 2. EUR 6M yield curves as observed on 2020-03-31 and 2020-12-31.

Table 1. Calibrated model parameters.

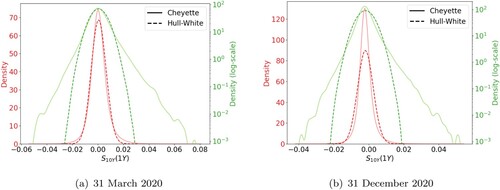

Figure 3. Risk-neutral densities of the 10Y swap rate after 1 year, displayed on a linear scale and a log scale. Plots are generated by calibrating the stochastic volatility Cheyette (solid) and the Hull–White (dashed) model to March 2020 (left) and December 2020 (right) data. (a) 31 March 2020 and (b) 31 December 2020.

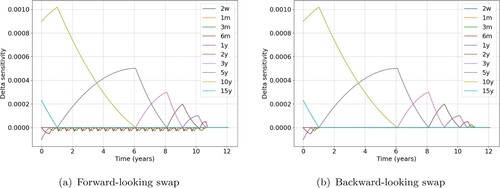

Figure 4. Delta Sensitivities under Hull–White (dashed) and Cheyette (solid) for a 1Yx10Y forward-looking (left) and backward-looking (right) interest rate swap. The results for the ATM derivative on 31 March 2020 are shown. (a) Forward-looking swap and (b) Backward-looking swap.

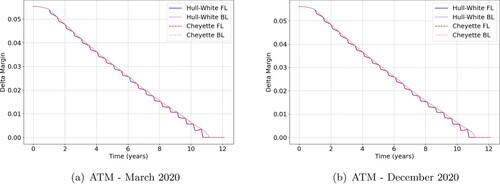

Figure 5. Delta margin under Hull–White (blue) and Cheyette (red) for a 1Yx10Y forward-looking (dark) and backward-looking (light) interest rate swap. Results for 31 March 2020 (left) and 31 December 2020 (right) are shown. (a) ATM – March 2020 and (b) ATM – December 2020.

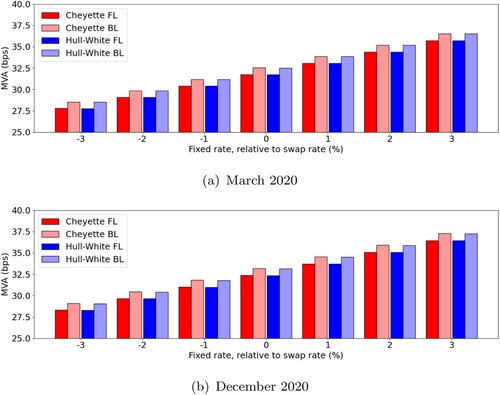

Figure 6. MVA charges under Hull–White and Cheyette for a 1Yx10Y forward-looking (dark) and backward-looking (light) interest rate swap. Results for 31 March 2020 (up) and 31 December 2020 (down) are shown for different levels of moneyness (). (a) March 2020 and (b) December 2020.

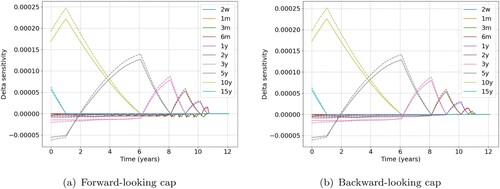

Figure 7. Delta sensitivities under Hull–White (dashed) and Cheyette (solid) for a 1Yx10Y forward-looking (left) and backward-looking (right) interest rate cap. The results for the OTM derivative () on 31 March 2020 are shown. (a) Forward-looking cap and (b) Backward-looking cap.

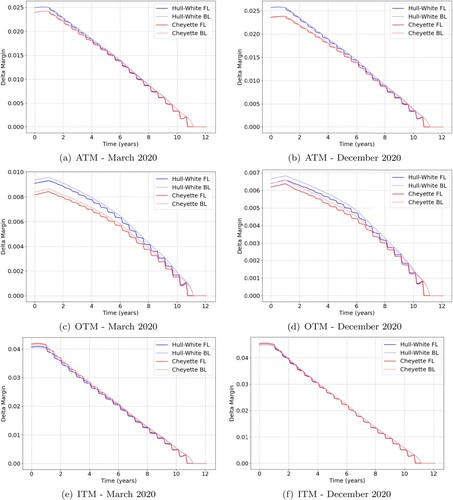

Figure 8. Delta margin under Hull–White and Cheyette for a 1Yx10Y forward-looking (dark) and backward-looking (light) interest rate cap. Results for 31 March 2020 (left) and 31 December 2020 (right) are shown for three different moneyness levels, namely ATM, OTM () and ITM (

). (a) ATM – March 2020. (b) ATM – December 2020. (c) OTM – March 2020. (d) OTM – December 2020. (e) ITM – March 2020 and (f) ITM – December 2020.

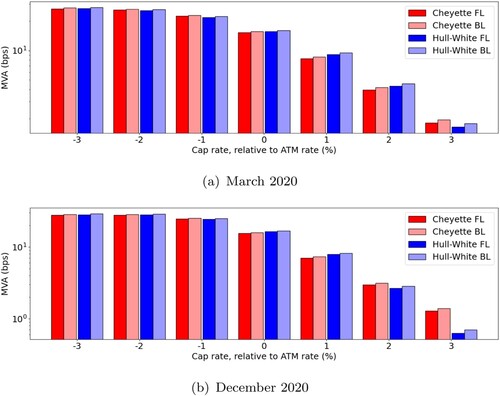

Figure 9. MVA charges associated with Delta margin under Hull–White and Cheyette for a 1Yx10Y forward-looking (dark) and backward-looking (light) interest rate cap. Results for 31 March 2020 (up) and 31 December 2020 (down) are shown for different levels of moneyness (). (a) March 2020 and (b) December 2020.

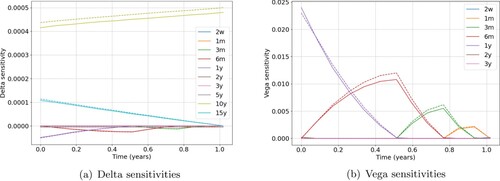

Figure 10. Delta (left) and Vega (right) sensitivities under Hull–White (dashed) and Cheyette (solid) for a 1Yx10Y swaption. The results for the ATM derivative on 31 March 2020 are shown. (a) Delta sensitivities and (b) Vega sensitivities.

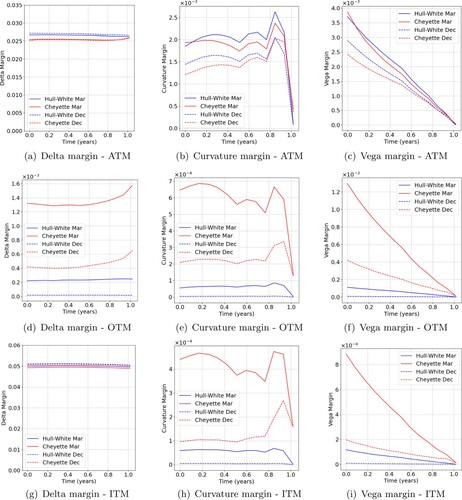

Figure 11. Delta (left), Curvature (middle) and Vega (right) margin under Hull–White and Cheyette for a 1Yx10Y swaption. Results for 31 March 2020 (solid) and 31 December 2020 (dashed) are shown for three different moneyness levels, namely ATM, OTM () and ITM (

). (a) Delta margin – ATM. (b) Curvature margin – ATM. (c) Vega margin – ATM. (d) Delta margin – OTM. (e) Curvature margin – OTM. (f) Vega margin – OTM. (g) Delta margin – ITM. (h) Curvature margin – ITM and (i) Vega margin – ITM.

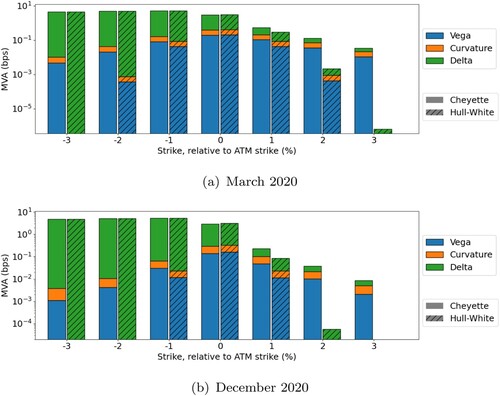

Figure 12. MVA charges under Hull–White (striped) and Cheyette (non-striped) for a 1Yx10Y swaption. Results for 31 March 2020 (up) and 31 December 2020 (down) are shown for different levels of moneyness (). (a) March 2020 and (b) December 2020.