Figures & data

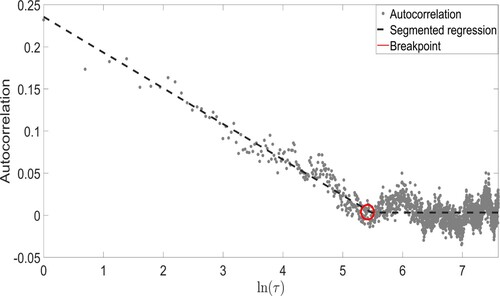

Figure 1. ACSR methodology computed on the autocorrelation function of the absolute values of the log-returns time series. The red circle shows the breakpoint where the regression line has a break.

Table 1. Results of the ACSR for the estimation of .

is the mean over all the paths and the

C.I. are computed over 200,000 bootstrapped samples.

Table 2. RMSE for the parameter A for the different methodologies.

Table 3. RMSE for the parameter B for the different methodologies.

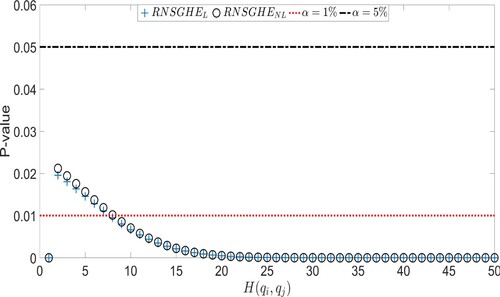

Figure 2. p-Values of all the 50 coefficients related to q moments equations for a multifractal random walk with T = 10, 000, , L = 250 and

.

Table 4. p-Values of the F-test for the null that only is different from 0.

Table 5. Summary statistics of the log-returns of the analyzed stocks.

Table 6. Results of the multiscaling estimation and testing procedure.

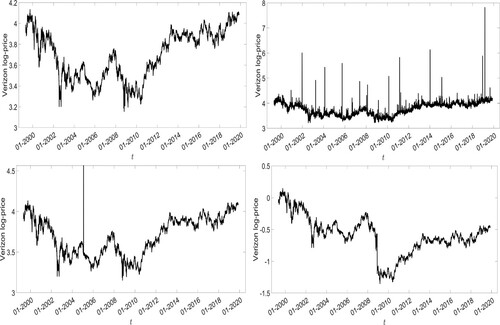

Figure 3. Verizon log-prices time series and some anomalies of financial time series.

Figure 4. Cumulative Variance (CV) and Cumulative Auto-Covariance (CAV) for the Verizon time series.

Figure 5. Cumulative Variance () and Cumulative Auto-Covariance (

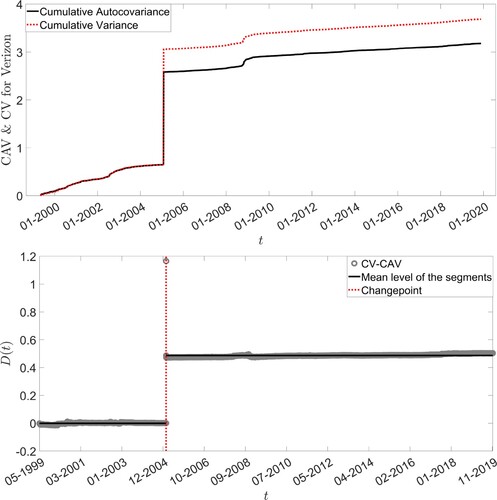

) for the Verizon time series (top panel) and the measure

(bottom panel) in case of the added spike.

Figure 6. Cumulative Variance () and Cumulative Auto-Covariance (

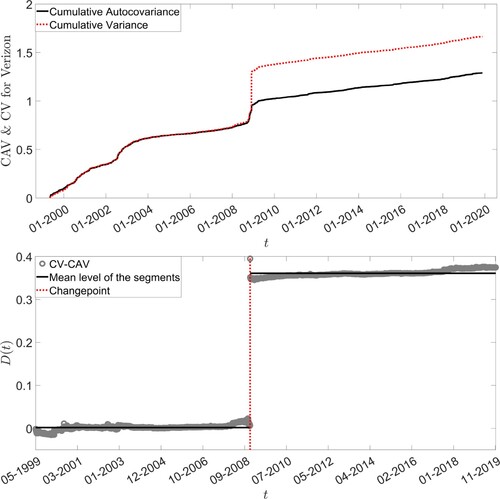

) for the Verizon time series (top panel) and the measure

(bottom panel) in case of the added jump.

Table 7. Results of the multiscaling estimation on the times series reported in Figure (bottom panels) with anomalies not removed.

Table 8. Average of the 100 estimated ,

and

for a fractional Brownian motion with H = 0.47.

C.I. computed over 200,000 bootstrapped samples are reported in parenthesis.

Table 9. Results of the jump detection analysis and estimated exponent parameters.

Figure 7. HVaR using annual data and using daily data rescaled by the factor and by

. Stocks are sorted by the magnitude of the annual Historical VaR.

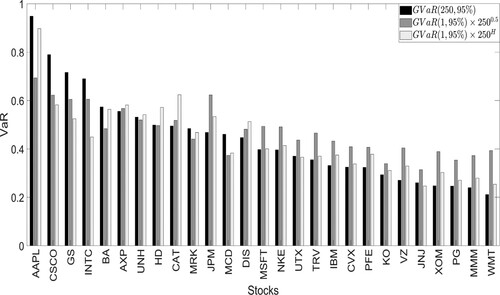

Figure 8. GVaR using annual data and using daily data rescaled by the factor and by

. Stocks are sorted by the magnitude of the annual Gaussian VaR.

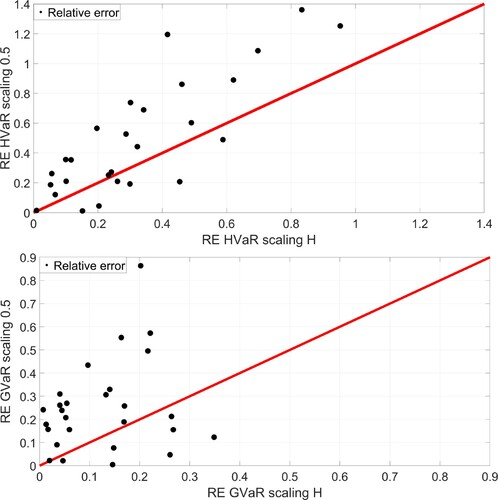

Figure 9. Relative error between the true VaR calculated using annual data, HVaR and GVaR computed using daily data scaled by the factor 0.5 and by the estimated factor H. The red line is the 45 degrees reference line.

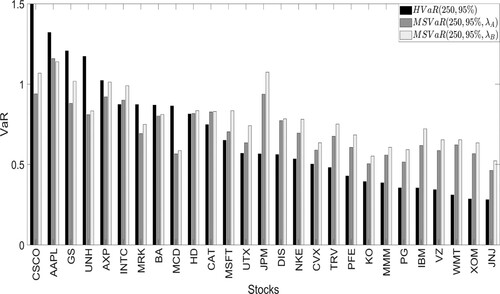

Figure 10. Annual Historical VaR (HVaR) and Multiscaling VaR (MSVaR). Confidence level . Stocks are sorted according to the magnitude of the Historical VaR.