Figures & data

Table 1. Transaction hours for Borsa Istanbul.

Table 2. Public holidays.

Table 3. Descriptive statistics of RV in the non-crisis period and the crisis period.

Table 4. Descriptive statistics of periodicity-adjusted jump tests.

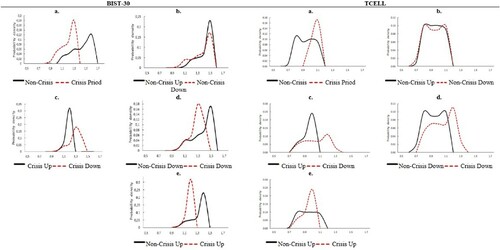

Figure 1. Realised volatility. This table shows realised volatility for BIST-30 and individual stocks in the non-crisis periods and the crisis period. Individual stocks are TCELL, VSTEL and SNPAM, which represent big, medium and small stocks respectively. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

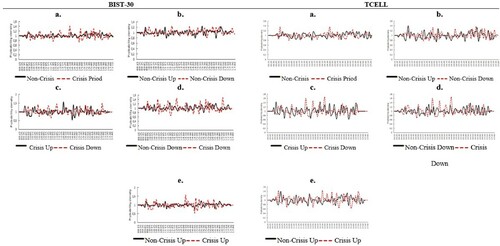

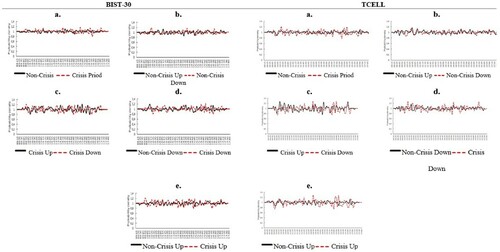

Figure 2. Intraday realised volatility. This table shows intraday realised volatility from 9.15 to 17.40 for BIST-30 and individual stocks in the non-crisis periods and the crisis period. Individual stocks are TCELL, VSTEL and SNPAM, which represent big, medium and small stocks respectively. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

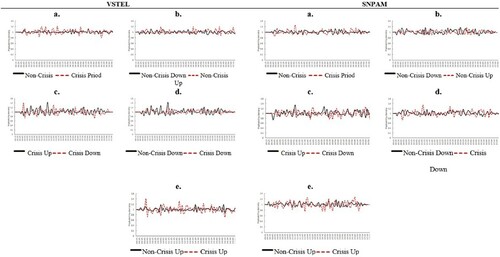

Figure 3. Intraday periodicity-adjusted jump statistics. This table shows summary statistics of the periodicity-adjusted intraday jump tests of Andersen, Bollerslev, and Diebold (Citation2007b) for BIST-30 and individual stocks in the non-crisis periods and the crisis period. Individual stocks are TCELL, VSTEL and SNPAM, which represent big, medium and small stocks respectively. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

Figure 4. Sample distribution of SW statistics. This figure shows the distribution of the non-standardised statistics for Brownian motion given by Sw for BIST-30 and TCELL, which represent the stock market index and big stocks respectively in the non-crisis periods and the crisis period. The table is obtained by computing the Sw, using values of k=2, α=2, and 1≤p≤1.75, taking into account asymmetry effects. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

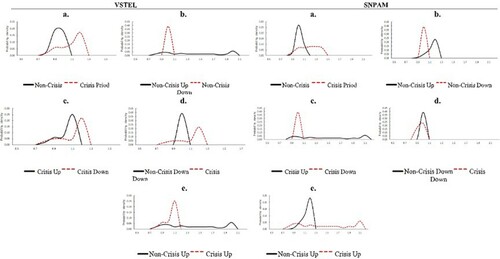

Figure 5. Sample distribution of SW statistics. This figure shows the distribution of the non-standardised statistics for Brownian motion given by Sw for VSTEL and SNPAM, which represent medium and small stocks respectively in the non-crisis periods and the crisis period. The table is obtained by computing the Sw, using values of k=2, α=2, and 1≤p≤1.75, taking into account asymmetry effects. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

Figure 6. Intraday distribution of SW statistics. This figure shows the intraday distribution of the non-standardised statistics for Brownian motion given by Sw for BIST-30 and TCELL, which represent the stock market index and big stock respectively in the non-crisis periods and the crisis period. The table is obtained by computing the Sw, using values of k=2, α=2, and 1≤p≤1.75, taking into account asymmetry effects. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

Figure 7. Intraday distribution of SW statistics. This figure shows the intraday distribution of the non-standardised statistics for Brownian motion given by Sw for VSTEL and SNPAM, which represent medium and small stocks respectively in the non-crisis periods and the crisis period. The table is obtained by computing the Sw, using values of k=2, α=2, and 1≤p≤1.75, taking into account asymmetry effects. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

Figure 8. Sample distribution of Sj statistics. This figure shows the distribution of the non-standardised statistics for the presence of jumps given by Sj for BIST-30 and TCELL, which represent the stock market index and big stock in the non-crisis periods and the crisis period. The table is obtained by computing the Sj, using values of k=2, α=8, and 2≤p≤6, taking into account asymmetry effects. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

Figure 9. Sample distribution of Sj statistics. This figure shows the distribution of the non-standardised statistics for the presence of jumps given by Sj for VSTEL and SNPAM, which represent medium and small stocks respectively in the non-crisis periods and the crisis period. The table is obtained by computing the Sj, using values of k=2, α=8, and 2≤p≤6, taking into account asymmetry effects. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

Figure 10. Intraday distribution of Sj statistics. This figure shows the intraday distribution of the non-standardised statistics for the presence of jumps given by Sj for BIST-30 and TCELL, which represent the stock market index and big stock in the non-crisis periods and the crisis period. The table is obtained by computing the Sj, using values of k=2, α=8, and 2≤p≤6, taking into account asymmetry effects. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

Figure 11. Intraday distribution of Sj statistics. This figure shows the intraday distribution of the non-standardised statistics for the presence of jumps given by Sj for VSTEL and SNPAM, which represent medium and small stocks respectively in the non-crisis periods and the crisis period. The table is obtained by computing the Sj, using values of k=2, α=8, and 2≤p≤6, taking into account asymmetry effects. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

Figure 12. Sample distribution of SFA statistics. This figure shows the distribution of the non-standardised statistics that distinguish between finite and infinite jumps given by SFA for BIST-30 and TCELL, which represent big stocks in the non-crisis periods and the crisis period. The table is obtained by computing the SFA, using values of k=2, α=8, and 2≤p≤6, taking into account asymmetry effects. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

Figure 13. Sample distribution of SFA statistics. This figure shows the distribution of the non-standardised statistics that distinguish between finite and infinite jumps given by SFA for VSTEL and SNPAM, which represent medium and small stocks respectively in the non-crisis periods and the crisis period. The table is obtained by computing the SFA, using values of k=2, α=8, and 2≤p≤6, taking into account asymmetry effects. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

Figure 14. Intraday distribution of SFA statistics. This figure shows the intraday distribution of the non-standardised statistics that distinguish between finite and infinite jumps given by SFA for BIST-30 and TCELL, which represent the stock market index and big stocks in the non-crisis periods and the crisis period. The table is obtained by computing the SFA, using values of k=2, α=8, and 2≤p≤6, taking into account asymmetry effects. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

Figure 15. Intraday distribution of SFA statistics. This figure shows the intraday distribution of the non-standardised statistics that distinguish between finite and infinite jumps given by SFA for VSTEL and SNPAM, which represent medium and small stocks respectively in the non-crisis periods and the crisis period. The table is obtained by computing the SFA, using values of k=2, α=8, and 2≤p≤6, taking into account asymmetry effects. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

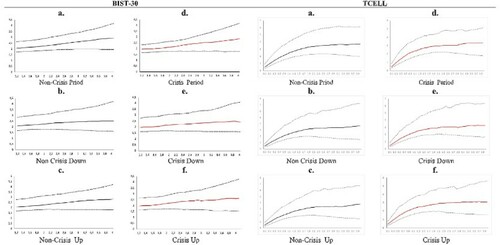

Figure 16. Activity signature plots. This figure shows quantile activity signature functions computed for BIST-30 and TCELL, which represent the stock market index and big stock respectively in the non-crisis periods and the crisis period. The table is obtained by computing the function using values of p for the quantiles using 0.25 (for lower bound), 0.50 (for median), and 0.75 for upper bound, taking into account asymmetry effects. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

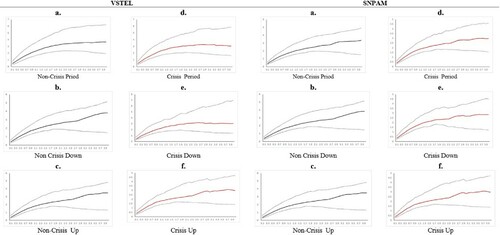

Figure 17. Activity signature plots. This figure shows quantile activity signature functions computed for VSTEL and SNPAM, which represent medium and small stocks respectively in the non-crisis periods and the crisis period. The table is obtained by computing the function using values of p for the quantiles using 0.25 (for lower bound), 0.50 (for median), and 0.75 for upper bound, taking into account asymmetry effects. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

Table 5. The proportion of quadratic variation.

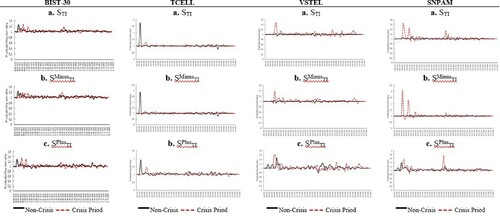

Figure 18. The distribution of STI, SMinusTI, and SPlusTI statistics. This figure shows the distribution of the non-standardised statistics for the presence of large jumps given by STI, SMinusTI, and SPlusTI for TCELL, VSTEL and SNPAM, which represent big, medium and small stocks respectively in the non-crisis periods and the crisis period. The table is obtained by computing the statistics of STI, SMinusTI, and SPlusTI, using values of 2.1≤p≤6, α=2, and k=2. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

Table 6. The Kolmogorov-Smirnov (KS) test.

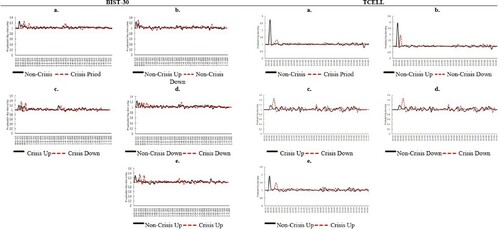

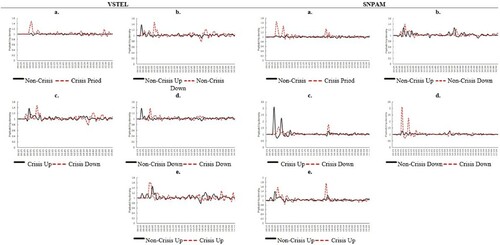

Figure 19. This figure shows the intraday distribution of the non-standardised statistics for the presence of large jumps given by STI, SMinusTI, and SPlusTI for TCELL, VSTEL and SNPAM, which represent big, medium and small stocks respectively in the non-crisis periods and the crisis period. The table is obtained by computing the statistics of STI, SMinusTI, and SPlusTI, using values of 2.1≤p≤6, α=2, and k=2. The data sample ranges from January 1, 2005 to December 31, 2013, including 2,268 trading days. The intraday interval is five minutes. The crisis period considered in this paper is from July 19, 2007 to May 29, 2009.

Table 7. Stressful days for absolute tail.

Table 8. Stressful days for positive tail.

Table 9. Stressful days for negative tail.

Data availability statement

The data that support the findings of this study are available from the corresponding author upon reasonable request.