Figures & data

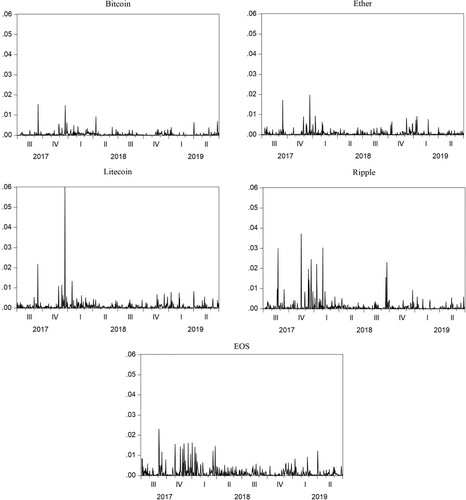

Figure 1. Cryptocurrencies’ total jumps.

Note: This Figure depicts the jumps in the five cryptocurrencies considered, namely Bitcoin, Ether, Litecoin, Ripple, and EOS, for the period from 1st July 2017–30th June 2019 (730 observations).

Table 1. Descriptive statistics of total jump series.

Table 2. Effects of jumps in Bitcoin on jumps in altcoins.

Table 3. Effects of jumps in altcoins on jumps in Bitcoin.

Table 4. Effects of jumps in altcoins on jumps in Ether.

Table 5. Effects of jumps in altcoins on jumps in Ripple.

Table 6. Effects of jumps in altcoins on jumps in Litecoin.

Table 7. Effects of jumps in altcoins on jumps in EOS.

Table 8. Asset allocation based on the Sortino ratio.

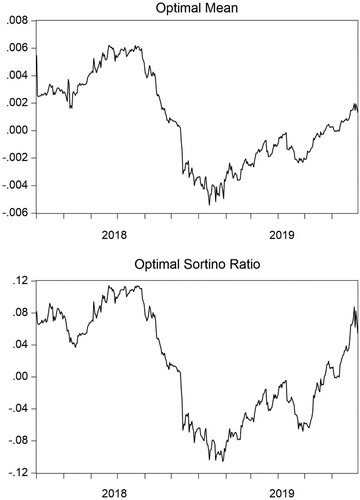

Figure 2. Optimal mean and Sortino ratio in a rolling window.

Note: These Figures depict the optimal mean portfolio return and optimal Sortino ratio of the portfolio consisting of the five cryptocurrencies considered, namely Bitcoin, Ether, Litecoin, Ripple, and EOS, in a rolling window application for the period from 1st July 2018–30th June 2019 (365 observations).

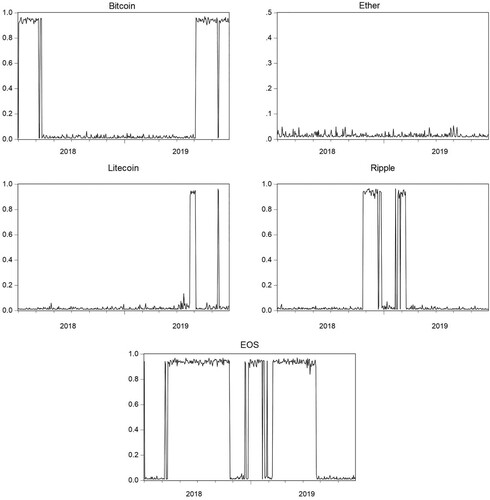

Figure 3. Weights of the optimal portfolio in a rolling window.

Note: This Figure depicts the weights of the optimal portfolio consisting of the five cryptocurrencies considered in our study, namely Bitcoin, Ether, Litecoin, Ripple, and EOS, in a rolling window application for the period from 1st July 2018–30th June 2019 (365 observations).

Table 9. Effects of jumps in the S&P 500 equity index on jumps in cryptocurrencies.