Figures & data

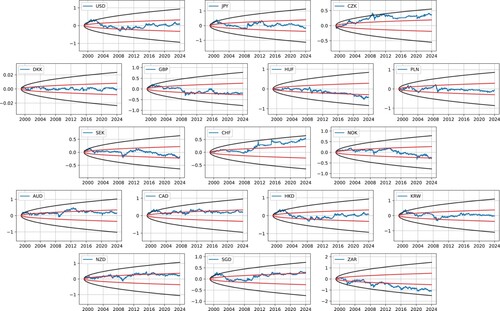

Figure 1. Log returns of the exchange rates of selected currencies in terms of EUR, where the black region is 95% confidence interval and the red region is the 50% confidence interval as implied by the market volatility. Note that the log returns of most currencies stay in the tighter 50% confidence interval, indicating slight mean reversion. Several currencies exhibit a drift: CZK, HUF, CHF, and ZAR.

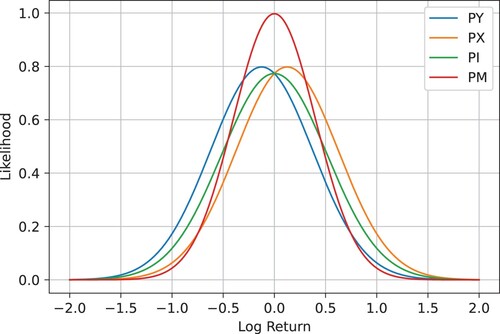

Figure 2. Distributional opinions about the final value of the log return from the perspective of the two currencies

and

, their index

, and the subjective agent's opinion

with parameters

,

, and T = 25.

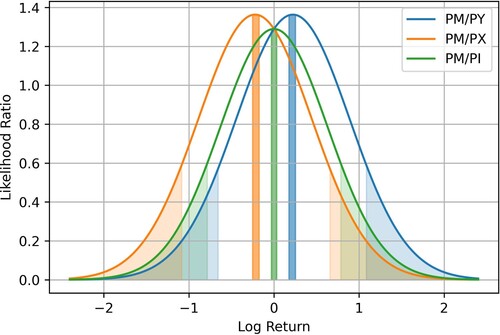

Figure 3. Likelihood ratios corresponding to the final log return of the subjective agent's opinion

against three available benchmarks:

,

, and

from Figure together with the rejection regions based on the Neyman-Pearson lemma. The central regions reject the state price density of the reference currency, the tail regions reject the state price density of the agent.

Table 1. Final log return as the test statistics of the exchange rate together with the rejection regions corresponding to all 3 different benchmarks. FX rates of currencies in bold stayed statistically significant around zero.

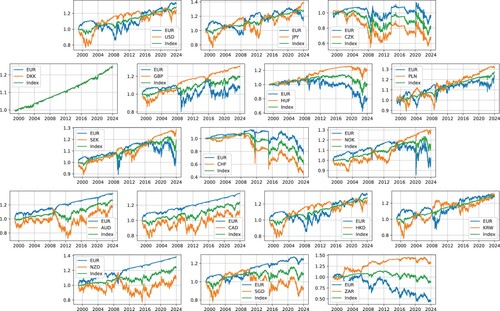

Table 2. Optimal values of the portfolios as a result of log utility maximization denominated in the index of two currencies, EUR, and the foreign currency.

Figure 4. The time evolution of the optimal value function for all currencies benchmarked with respect to EUR (blue graph), the other currency (orange graph), and the index of the two currencies (green graph). The choice of the scaling factor a in is 0.8.

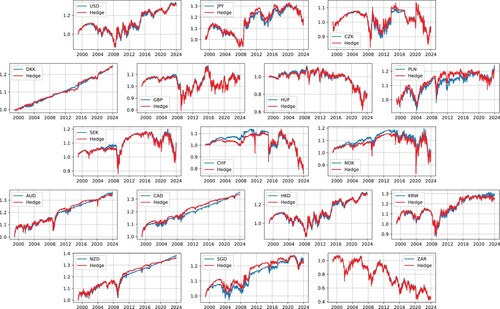

Figure 5. Comparison of the EUR theoretical optimal value function (blue) with its replicating portfolio (red).

Table 3. Annualized Sharpe ratio.

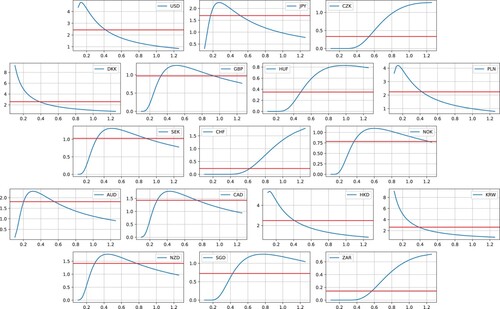

Figure 6. The performance of individual funds as a function of the scaling parameter a for different currencies denominated in EUR. Currencies with smaller variability peak for values under a = 1. The red line corresponds to the mean performance of the funds sampled from the distribution for the scaling factor a.

Table 4. Cumulative performance of the Bayesian portfolios.

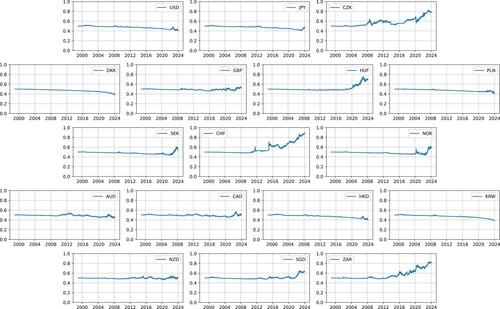

Figure 7. Temporal evolution of the mean posterior for the scaling factor parameter a.

Data Availability Statement

The data that support the findings of this study are openly available in the European Central Bank repository at https://www.ecb.europa.eu/stats/eurofxref/eurofxref-hist.zip, derived from the European Central Bank Exchange Rate Data.