Figures & data

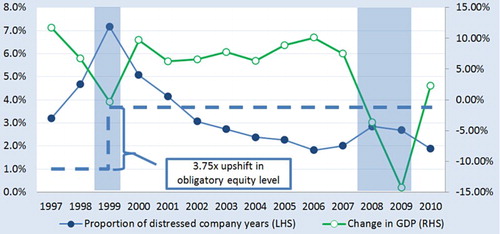

Figure 1. Distress episodes and real GDP growth.Notes: A firm was defined as distressed if it breached the minimum capital requirements set by law. The obligatory equity level has been EUR 2.4 thousand for private limited companies and EUR 24 thousand for public limited companies since 1999; in 1995–1998, the obligatory equity levels were EUR 0.64 thousand for private limited companies and EUR 6.4 thousand for public limited companies. Two shadowed areas denote the crises of 1999 and 2008–2009. The source for real GDP growth is Statistics Estonia (Citation2013).

Table 1. Summary statistics by sector.

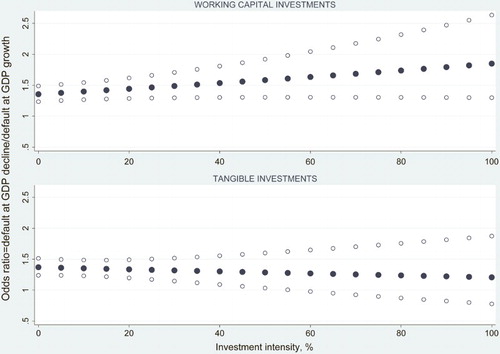

Figure 2. Odds ratios at different levels of investment intensity with 95% confidence intervals.

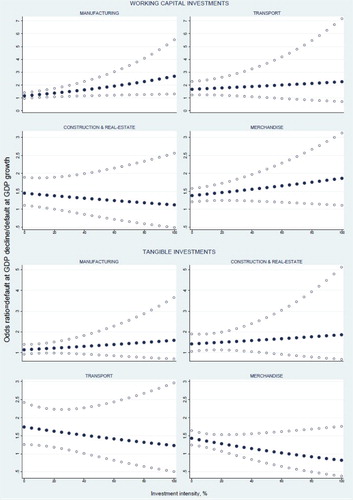

Figure 3. Odds ratios at different levels of investment intensity with 95% confidence intervals by industries.