Figures & data

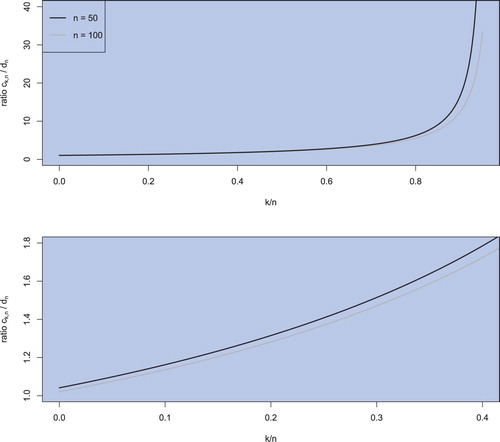

Figure 1. The ratio plotted as a function of k/n for

and

.

Table 1. Average absolute deviation (AD) of the estimated portfolio expected return and of the estimated portfolio variance from their population values.

Table 2. Average absolute deviation (AD) of the estimated portfolio expected return and of the estimated portfolio variance from their population values.

Table 3. Average absolute deviation (AD) of the estimated portfolio expected return and of the estimated portfolio variance from their population values.

Table 4. Average absolute deviation (AD) of the estimated portfolio expected return and of the estimated portfolio variance from their population values.

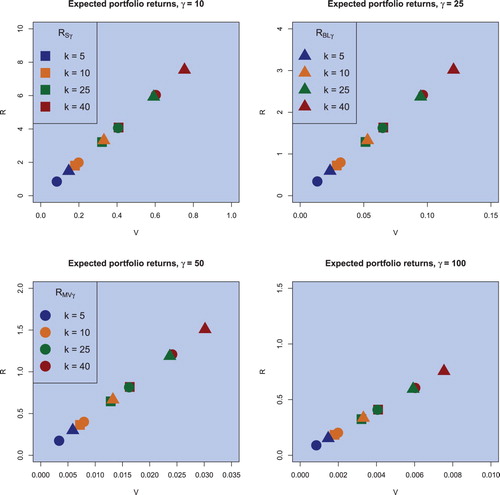

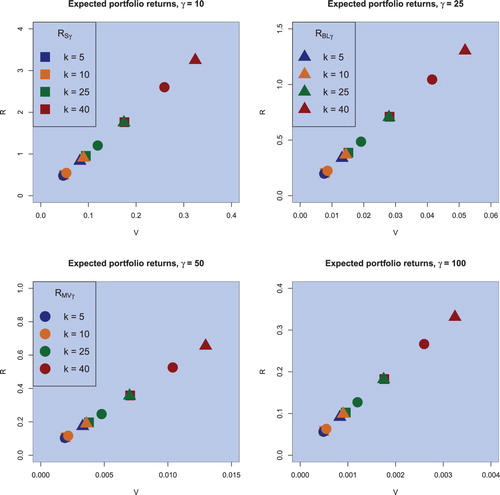

Figure 2. Sample optimal portfolios (squares), (objective) Bayesian optimal portfolios (circles), and the Black–Litterman optimal portfolios (triangulares) for the risk aversion coefficient of , for the sample case of n = 130 and for the portfolio dimension of

in the case of weekly data.

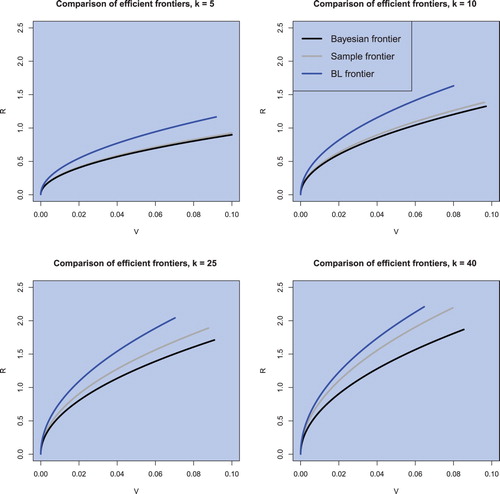

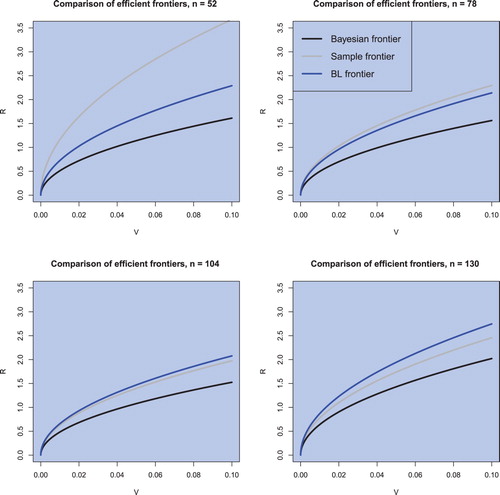

Figure 3. The sample efficient frontier, the (objective) Bayesian efficient frontier, and the Black–Litterman efficient frontier for n = 130 and in the case of weekly data.

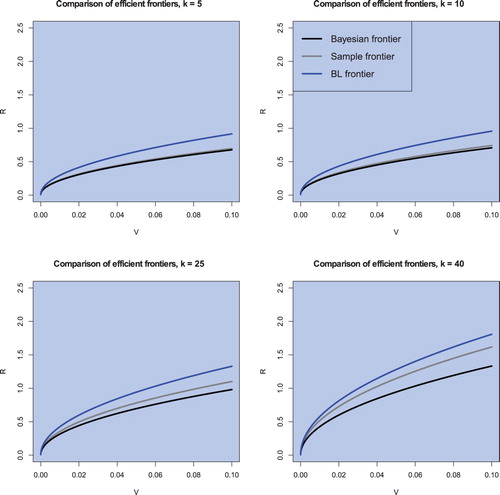

Figure 4. The sample efficient frontier, the (objective) Bayesian efficient frontier, and the Black–Litterman efficient frontier for k = 40 and in the case of weekly data.

Figure 5. Sample optimal portfolios (squares), (objective) Bayesian optimal portfolios (circles), and the Black–Litterman optimal portfolios (triangulares) for the risk aversion coefficient of , for the sample case of n = 130 and for the portfolio dimension of

in the case of monthly data.

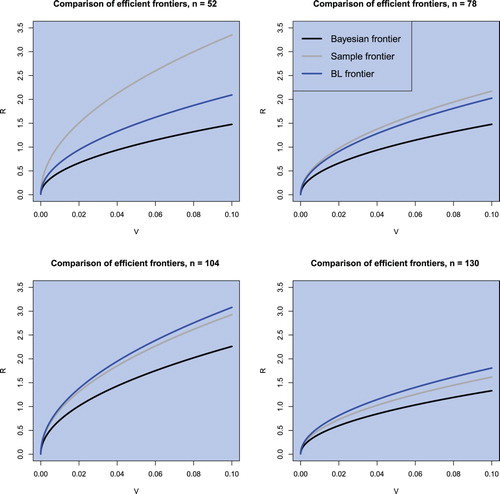

Figure 6. The sample efficient frontier, the (objective) Bayesian efficient frontier, and the Black–Litterman efficient frontier for n = 130 and in the case of monthly data.

Figure 7. The sample efficient frontier, the (objective) Bayesian efficient frontier, and the Black–Litterman efficient frontier for k = 40 and in the case of monthly data.

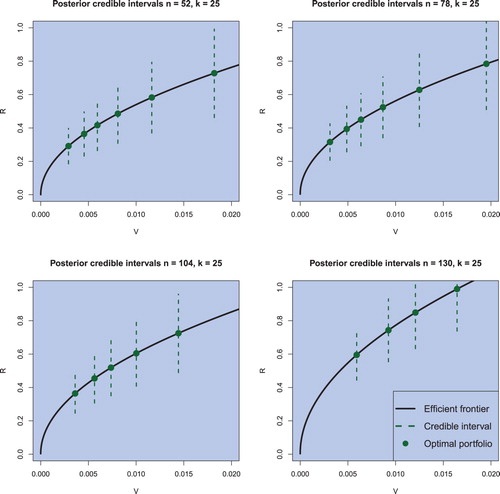

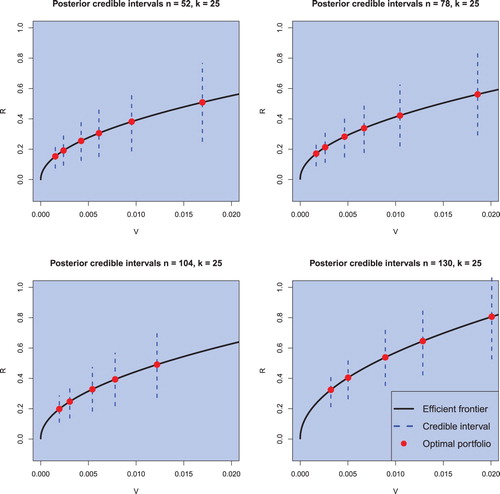

Figure 8. Credible intervals for the return of optimal portfolios with varying risk attitudes for weekly data obtained by employing the (objective) Bayesian approach. The sample sizes are chosen to be and the portfolio dimension is fixed to k = 25. The confidence level is set to

.

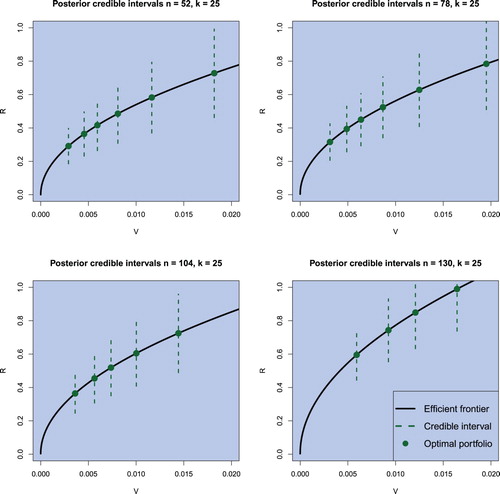

Figure 9. Credible intervals for the return of optimal portfolios for the Black–Litterman model with varying risk attitudes for weekly data. The sample sizes are chosen to be and the portfolio dimension is fixed to k = 25. The confidence level is set to

.

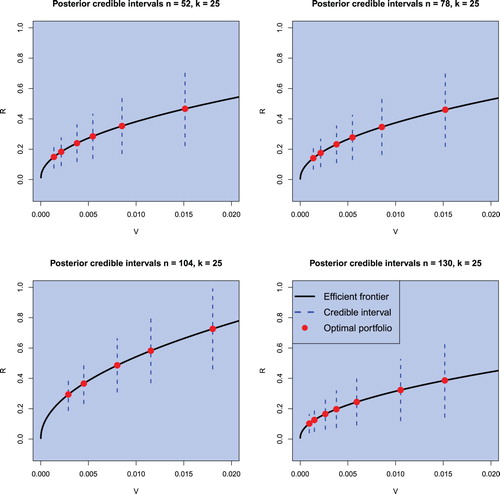

Figure 10. Credible intervals for the return of optimal portfolios with varying risk attitudes for monthly data obtained by employing the (objective) Bayesian approach. The sample sizes are chosen to be and the portfolio dimension is fixed to k = 25. The confidence level is set to

.

Figure 11. Credible intervals for the return of optimal portfolios for the Black–Litterman model with varying risk attitudes for monthly data. The sample sizes are chosen to be and the portfolio dimension is fixed to k = 25. The confidence level is set to

.