Figures & data

Figure 1. FTSE 100 Index. Centrality measures and portfolio weights. Panel (a) reports the relationship between asset centrality and the portfolio weights. To do this, the weights allocated to the assets comprising the FTSE 100 Index under the global minimum variance portfolio, see (Equation2(2)

(2) ), are ranked from smallest to largest and the associated centrality measure (Equation9

(9)

(9) ) is plotted. Panel (b) reports the relationship between asset centrality and the portfolio weights under short-selling constraints

.

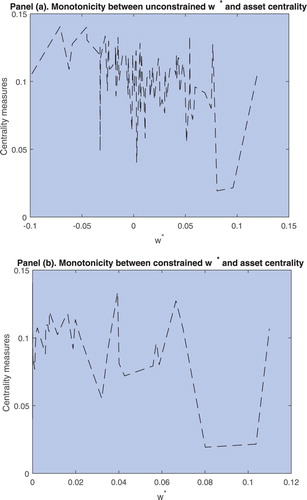

Figure 2. Random subsample of FTSE 100 Index. Centrality measures and portfolio weights. Each row contains a random subsample of 20 stock returns from the FTSE 100 Index such that the five rows span all the assets in the FTSE 100 Index. The left panel reports the relationship between asset centrality and the portfolio weights under the absence of short-selling constraints and the right panel reports such relationship imposing short-selling constraints ().

Table 1. Summary statistics. January 2011 to May 2020.

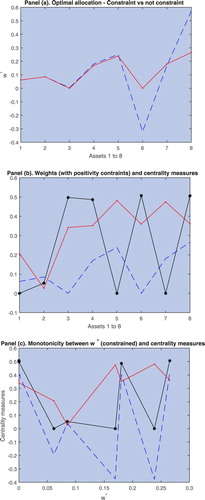

Figure 3. Static analysis of centrality measures and portfolio weights. Panels (a)–(f): the black solid line denotes the positive centrality measure (Equation10(10)

(10) ) and the red dashed line the negative measure (Equation11

(11)

(11) ). Panel (a): the green line denotes the centrality measure (Equation9

(9)

(9) ). Panel (b): the red line for the constrained portfolio and blue dashed line for the unconstrained portfolio. Panels (c)–(d): the blue dashed line denotes the optimal portfolio allocation for each asset. Panels (e)–(f): the blue dashed line denotes the centrality measure (Equation9

(9)

(9) ).

Figure 4. CCC model with constrained weights. The black solid line denotes the positive centrality measure (Equation10(10)

(10) ) and the red dashed line the negative centrality measure (Equation11

(11)

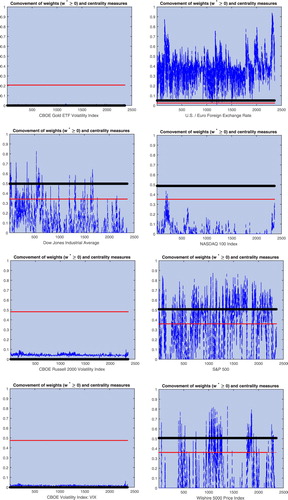

(11) ). The blue line denotes the dynamic optimal portfolio allocation over the evaluation period January 2011 to May 2020.

Figure 5. DCC model with constrained weights. The black solid line denotes the positive centrality measure (Equation10(10)

(10) ) and the red dashed line the negative centrality measure (Equation11

(11)

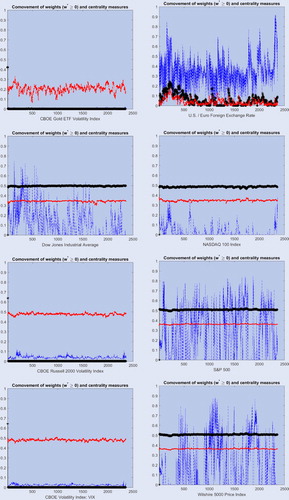

(11) ). The blue line denotes the dynamic optimal portfolio allocation over the evaluation period January 2011 to May 2020.

Table 2. Covariance and correlation matrix. January 2011 to May 2020.

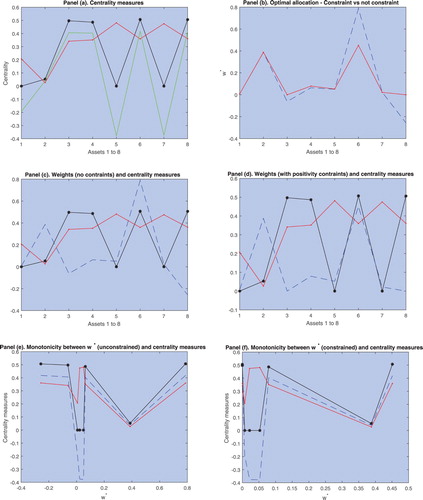

Figure 6. Static analysis of centrality measures and portfolio weights. Panel (a): the red line denotes the constrained portfolio and the blue dashed line the unconstrained portfolio. Panel (b): the black solid line denotes the positive centrality measure (Equation10(10)

(10) ) and the red dashed line the negative centrality measure (Equation11

(11)

(11) ). The blue dashed line denotes the optimal portfolio allocation for each asset. Panel (c): the black solid line denotes the positive centrality measure (Equation10

(10)

(10) ) and the red dashed line the negative centrality measure (Equation11

(11)

(11) ). The blue dashed line denotes the centrality measure (Equation9

(9)

(9) ).