Figures & data

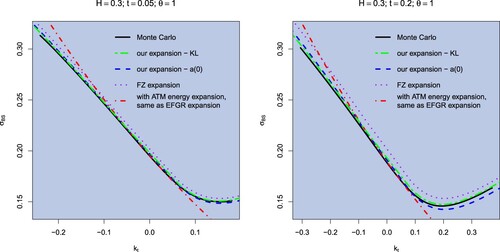

Figure 1. Implied volatility smile approximations for the rBergomi model with parameters , for expiry

. The Monte Carlo price is computed via the hybrid scheme for rBergomi in Bennedsen et al. (Citation2017) with

, with

simulations and 500 time steps of length t/500. The rate function is computed using the Ritz method in Section 5.1 with N = 8 Haar basis functions, the coefficient

is computed using the Karhunen–Loeve decomposition with N = 300 Haar basis functions (KL). We also compare with

expanded at 0 (

).

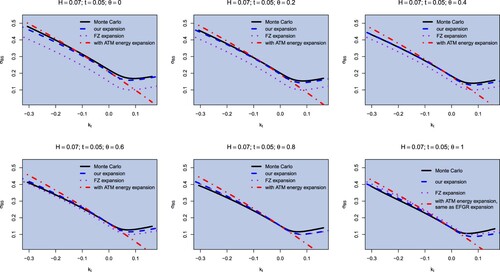

Figure 2. Implied volatility smile approximation for the rBergomi model with parameters , for expiry t = 0.05. The Monte Carlo price is computed via the hybrid scheme for rBergomi in Bennedsen et al. (Citation2017) with

, with

simulations and 500 time steps. The rate function is computed using the Ritz method with N = 9 Fourier basis functions.

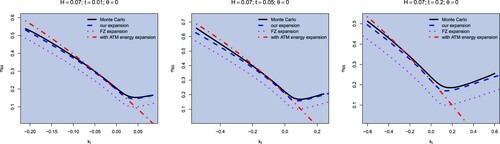

Figure 3. Implied volatility smile approximation for the rBergomi model with parameters , for expiry t = 0.01, 0.05, 0.2. The Monte Carlo price is computed via the hybrid scheme for rBergomi in Bennedsen et al. (Citation2017) with

, with

simulations and 500 time steps of length t/500. The rate function is computed using the Ritz method with N = 9 Fourier basis functions.

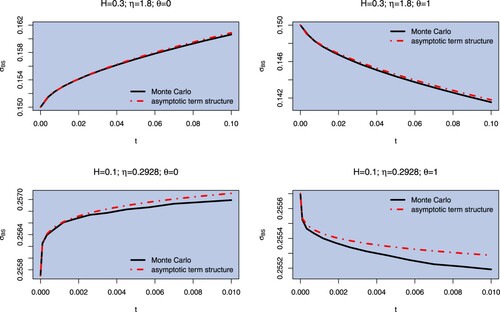

Figure 4. Term structure of volatility for the rBergomi model with parameters (above) and with parameters

(below). We plot ATM implied volatility as expiration time increases. We consider shorter expiries in the case of rougher trajectories (smaller Hurst parameter H; however, in this case we also take a smaller vol-of-vol parameter η). The Monte Carlo prices are computed via the hybrid scheme in Bennedsen et al. (Citation2017) with

, with

simulations and 500 time steps.

Figure 5. Moderate deviation with and x = 0.4 (time varying log-strike

) of implied volatility in rBergomi model with

. Simulation parameters:

simulation paths, 500 time steps. Time interval

.

![Figure 5. Moderate deviation with β=0.06 and x = 0.4 (time varying log-strike kt=xt1/2−H+β) of implied volatility in rBergomi model with σ0=0.2557,η=0.2928,ρ=−0.7571,H=0.1,θ=0. Simulation parameters: 108 simulation paths, 500 time steps. Time interval [0,0.1].](/cms/asset/e2b55de1-c477-46ef-8d90-ac58bddeb7ee/rquf_a_1999486_f0005_oc.jpg)