Figures & data

Table 1. Start dates of accounting and price data sets for different international indexes.

Table 2. Summary statistics on our sample of 72 factors. Annualised Sharpe ratio and t-stats were computed with monthly returns. All factors are beta-neutralised, computed on CRSP from 1963 to 2014.

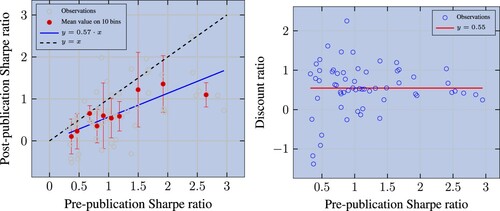

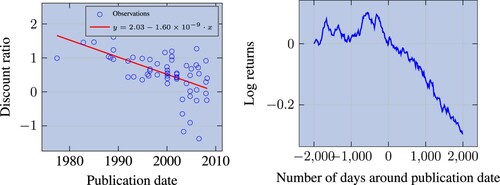

Figure 1. Left panel: Sharpe ratios of factors post-publication versus pre-publication. The regression is performed with OLS and has a of 67%. Observations are divided into deciles and we compute the average (resp. median) Sharpe ratio in-sample (resp. post-publication). The error bars show the standard deviation in the y direction. Right panel: Discount ratio versus pre-publication Sharpe ratio. The median discount ratio is 0.55.

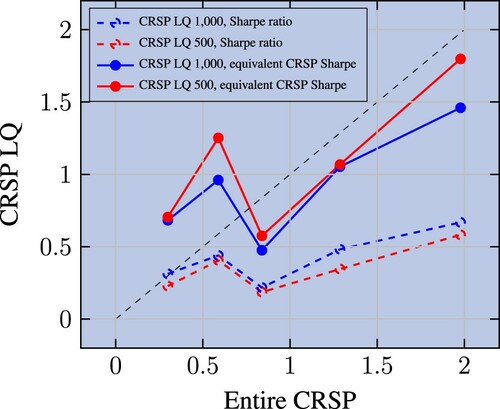

Figure 2. Raw and size-adjusted Sharpe ratios on liquidity pools vs. their original pool (as specified by the authors) counterparts. Observations are cut into five bins based on quantiles, we then compute the average (resp. median) Sharpe ratio on CRSP (resp. CRSP LQ 1000 or 500). Factors are beta-neutralised and Sharpe ratios below 0.3 on the entire CRSP universe (in-sample) are excluded.

Table 3. Median discount ratio.

Table 4. Statistics for arbitrage variables before standardization. We only retain strategies with an in-sample Sharpe ratio on CRSP higher than 0.3.

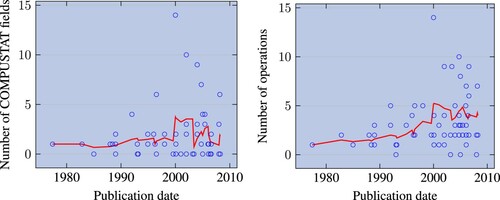

Figure 3. Number of Compustat fields (resp. operations) used to compute the factors' characteristic, as a function of publication date. We only show factors whose in-sample Sharpe ratio is greater than 0.3. One dot per factor. The red line represents a moving average of five factors.

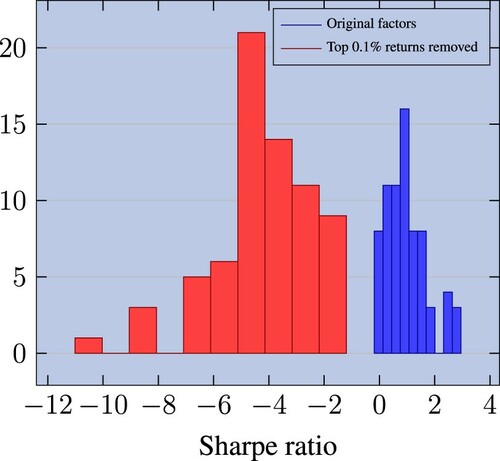

Figure 4. Distribution of in-sample Sharpe ratios of factors. We show original factors and a version where we remove the top 0.1% portfolio returns (Broderick et al. Citation2021). All 72 factors are beta-neutralised.

Table 5. Stats for overfitting variables before standardization. We only retain strategies with an in-sample Sharpe ratio on CRSP higher than 0.3.

Figure 5. Left panel: discount ratio as a function of publication date. Factors are beta-neutralised and computed on CRSP and we only retain those with Sharpe ratio greater than 0.3; one dot per factor; the red line draws a linear trend, fitted on blue dots, where dates are represented in Unix time. Right panel: average PnL of factors, centered on publication date; the average PnL is detrended based on the pre-publication period; factors are market-neutralised and, to be comparable, risk-managed; we use with the original stock pool and eliminate strategies that do not replicate well in sample.

Table 6. OLS univariate regressions of the discount ratio on arbitrage variables (t-stats in parentheses).

Table 7. OLS univariate regressions of the discount ratio on overfitting variables (t-stats in parentheses).

Table 8. OLS regressions with arbitrage and overfitting vulnerabilities.

Table A1. List of factors and the corresponding references.

Table A2. OLS regressions of equivalent Sharpe ratio of CRSP LQ 500 (resp. 1000) on CRSP (t-stats in parenthesis).

Table A3. Correlation matrix for arbitrage variables.

Table A4. Correlation matrix for overfitting variables; dts = dummy tstat, lqscv = log q span cv, dbq = diff from best q, dnf = dumy nb fields, dno = dummy nb operations, snm = sqrt nb months is, lss = log std subset, ddd = diff w drop data.

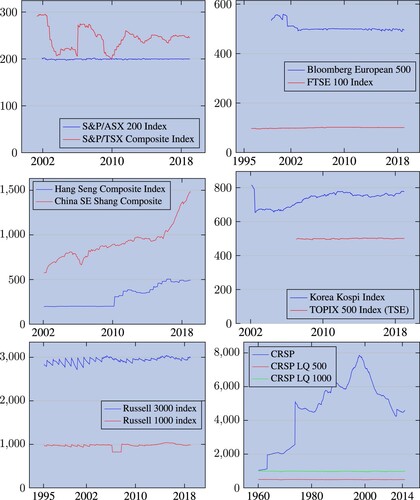

Figure A1. Number of constituents in each pool.

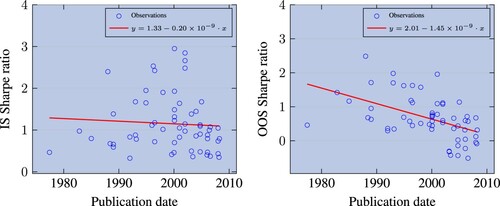

Figure A2. In-sample (resp. out-of-sample) Sharpe ratio as a function of publication date. Factors are beta-neutralised and computed on CRSP, conditional on its in-sample Sharpe ratio being greater than 0.3. One dot per factor. The red line draws a linear trend, fitted on blue dots, where dates are represented in Unix time. The are 0.4% and 24% respectively.