Figures & data

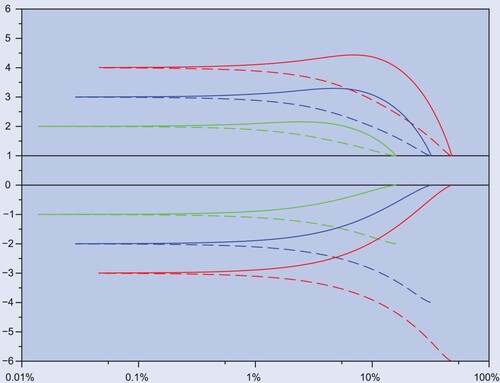

Figure 1. Buy (dashed) and sell (solid) boundaries (vertical, as risky weights π) versus average tracking error (horizontal) for leveraged (top) and inverse (bottom) funds, with multipliers 4 (top), 3, 2,

,

,

(bottom). As aversion to tracking error γ decreases from left (

) to right (

), for inverse funds (bottom) the trading boundaries widen around the target, whereas for leveraged funds (top) they first widen and then collapse to one.

and zero risk premium.

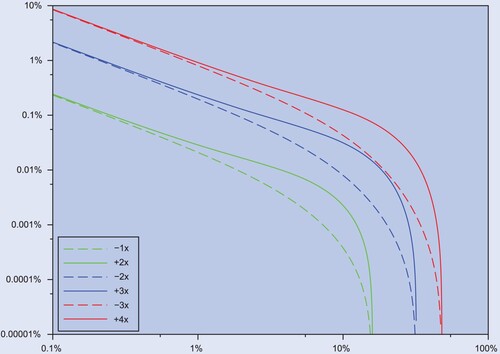

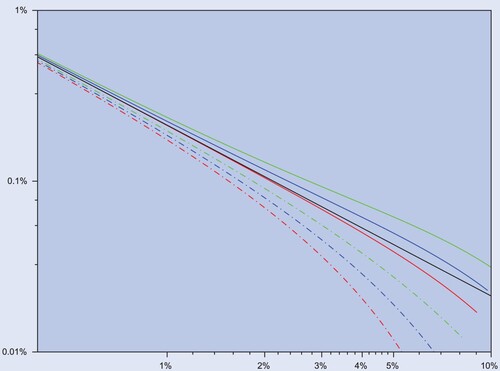

Figure 2. Negative tracking difference (, vertical) against tracking error (horizontal) for leveraged (solid) and inverse (dashed) funds, in logarithmic scale, from −3, +4 (top), to −2, +3 (middle), and −1, +2 (bottom). As aversion to tracking error γ decreases from left (

) to right (

), a k + 1-leveraged fund is akin to a

inverse one, as the respective curves (same color) approach low and high

aversion.

,

, and zero risk premium.

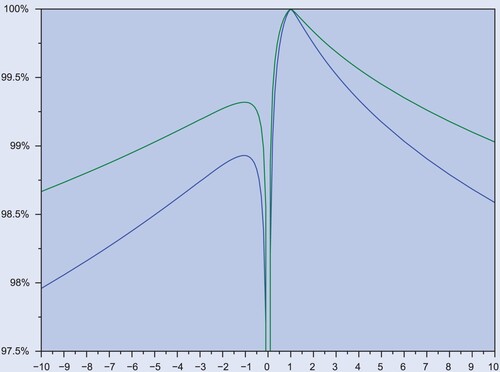

Figure 3. Exact (vertical) for inverse and leveraged factors Λ (horizontal), with aversion parameter

(blue) and

(green).

Table 1. Average exposure (left) and average daily turnover (right), both as percent of funds' values, in different asset classes for S&P 500 LIETFs: SPXU (−3), SDS (−2), SH (−1), SSO (+2), UPRO (+3), from 2018-01-26 to 2018-04-06.

Table 2. Summary statistics for the ratio (as percent) between (i) daily volume generated by LIETFs on the S&P 500 and (ii) daily volume in the S&P 500 components. Data from 2009-06-23 to 2018-03-27.

Table 3. Performance of LIETFs on selected indexes through December , 2022. For each index, observations begin on the earliest date for which all inverse (−3, −2, −1) and leveraged (2, 3) multiples are available. (Earliest date is November

, 2008.) Historical prices from Yahoo Finance, Interest rates from US Treasury.

Table 4. Average exposure () for typical factors (Λ) across trading costs (ε) and

aversion (γ), obtained from equation (Equation22

(22)

(22) ).

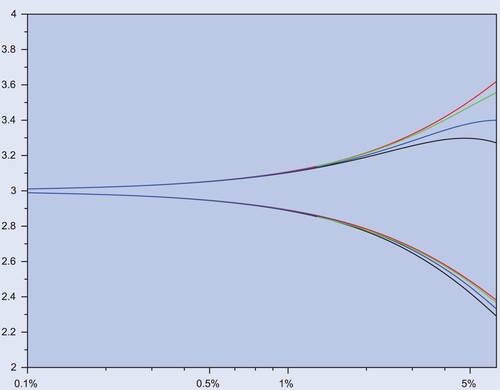

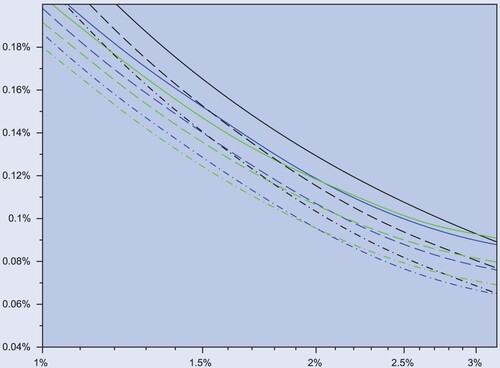

Figure 4. Trading boundaries (vertical) for factor against tracking error (horizontal), from first-order asymptotics (Equation25

(25)

(25) ) (red) and exact solutions for

(black),

(blue), and

(green). For realistic levels of tracking error, the impact of κ is of second order.

Figure 5. Negative tracking difference () for

leveraged fund (vertical, colored solid lines) and

(dashed colored lines), against tracking error (TrE) (horizontal), for

(black),

(blue) and

(green). The solid red line represents the asymptotic formula in (Equation1

(1)

(1) ), which is the same for L and 1−L.

Figure 6. Negative tracking difference () for a

leveraged fund (vertical), against tracking error (horizontal), for

(solid lines), 1.5625 (dashed) and 3.125 (dashed-dotted), when

. The black lines depicts the exact performance from (Equation26

(26)

(26) ) with

. The blue and green lines correspond to Monte Carlo Estimates (15000 paths, daily grid) for the Black–Scholes (blue) and Heston (green) models, with time horizon of T = 5 years, daily sampling and trading frequency, and correlation

.

Data Availability Statement

The code and data supporting this paper's findings are at https://github.com/guasoni/leveraged-funds.