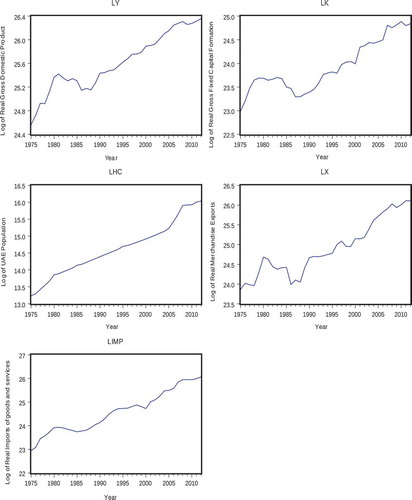

Figures & data

Table 1. Descriptive statistics of the series for the period 1975–2012

Table 2. ADF, PP and SL test results at logarithmic level

Table 3. ADF, PP and SL test results at first difference

Table 4. Johansen’s cointegration test results

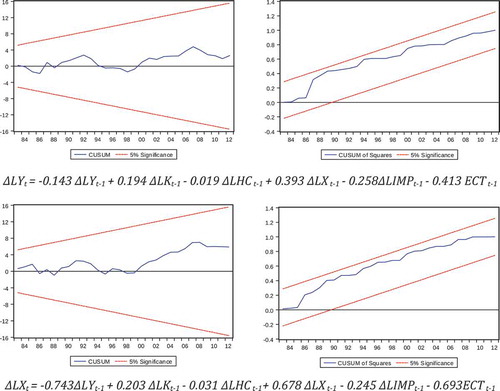

Table 5. DOLS estimation results (EquationEquation 8) (8) (8)

(8) (8)

Table 6. DOLS estimation results (EquationEquation 9)(9) (9)

Table 7. Short-run Granger causality test

Table 8. Causality based on the Toda-Yamamoto procedure

Table A1. Johansen’s cointegration test with one structural break (year: 1986)

Table A2. Johansen’s cointegration test with two structural breaks (years: 1986, 2001)