Figures & data

Table 1. Crisis dates.

Figure 1. Posterior mean of latent banking crisis indicator with end-of sample forecasts and 68 percent probability interval.

Figure 3. Forecast error variance decomposition by sector for each country.

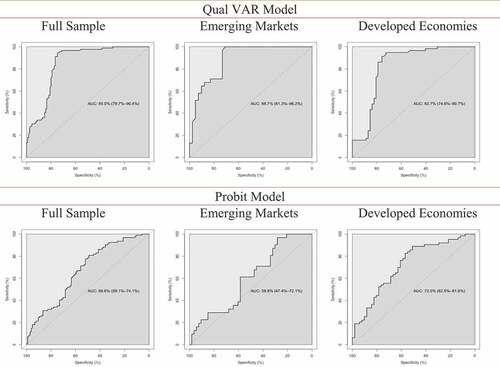

Figure 4. Out-of-sample forecasts: ROC curves.

Figure 2. Posterior mean of latent banking crisis indicator with end-of sample forecasts and 68 percent (95 percent where specified) probability interval: Robustness check.

Table 2. Out-of-sample forecasts of banking crisis probabilities.

Table 3. In-sample probit forecasts.

Table 4. Out-of-sample Qual VAR forecasts.

Table 5. Out-of-sample probit forecasts.

Table 6. Out-of-sample forecasts: AUROC results.

Table A1. Variables and transformations.

Table A2. Unit-root tests.

Table A3. Out-of-sample prediction dates.

Table A4. Out-of-sample forecasts of banking crisis probabilities: robustness check.

Table A5. Probit model results.