Figures & data

Table 1. Contingency table of fisher’s exact test for VaR measures in different periods

Table 2. Stock exchanges and the respective indices used

Table 3. GSADF tests for the log price–dividend ratio and log dividend difference in the nine markets

Table 4. Bubble periods obtained by the PSY test and the modified date-stamping method

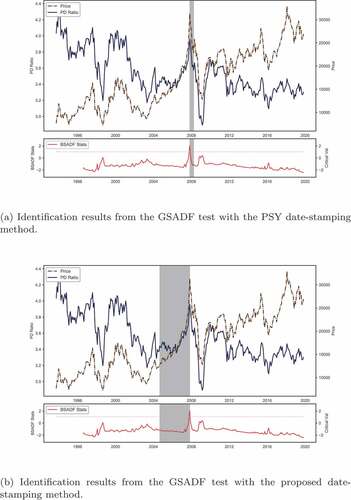

Figure 1. Bubble identification results for the hong kong stock market.

Table 5. Full, pre-bubble, bubble, post-burst, and normal periods for the bubbles examined in the nine stock markets

Table 6. Backtest results of riskmetrics VaR in the pre-bubble, bubble, and post-burst periods

Table 7. Backtest results of riskmetrics VaR in the normal and full periods

Table 8. Backtest Results of RiskMetrics 2006 VaR in the Pre-bubble, Bubble, and Post-burst Periods

Table 9. Backtest results of riskmetrics 2006 VaR in the full and normal periods

Table 10. Fisher exact test for the significance level of the difference of VaR failure rate by time period