Figures & data

Figure 1. More regional trade.

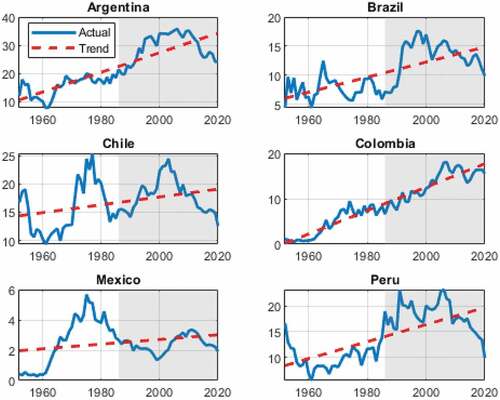

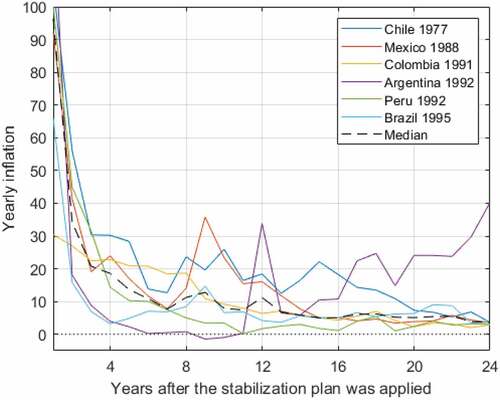

Figure 2. Improved macroeconomic outcome.

Table 1. Deeper financial integration

Table 2. Higher exchange rate correlations

Table 3. Stronger business cycles correlations

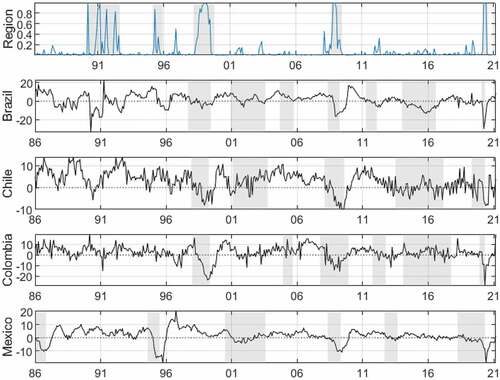

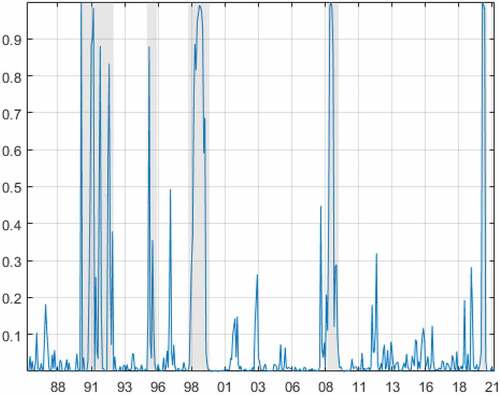

Figure 3. Regional recession probabilities.

Figure 4. Industrial production yearly growth rates and regional recessions.

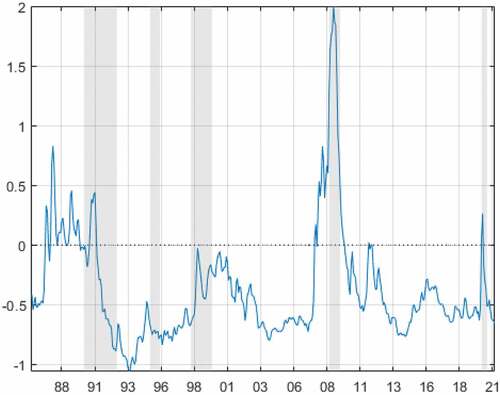

Figure 5. US financial conditions index.

Figure 6. Total connectedness (%), 5 year rolling window.

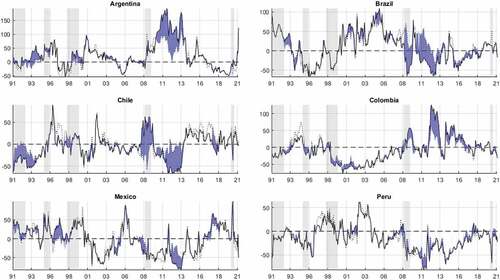

Figure 7. Net group connectedness (%), 5 year rolling window.

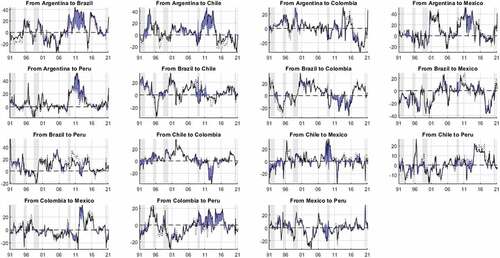

Figure 8. Net pairwise connectedness (%), 5 year rolling window.

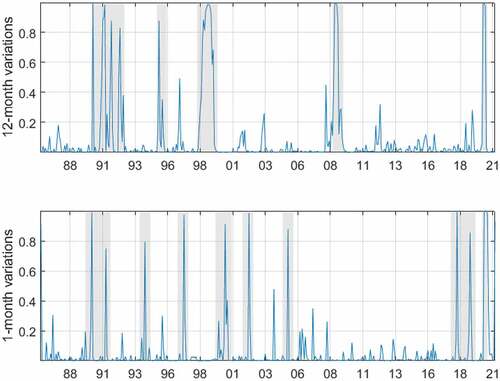

Figure A1. Regional recession probabilities, 12- and 1-month IPI variations.

Figure A2. 1-month IPI variations and regional recessions.

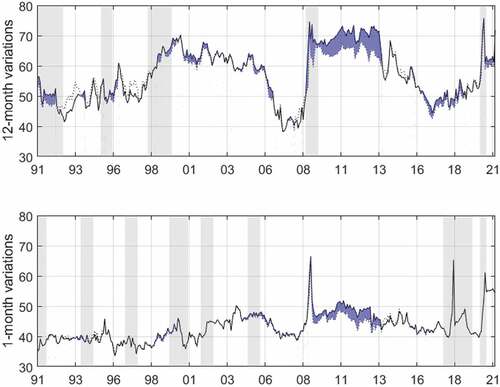

Figure A3. Total connectedness (%), 5 year rolling window, 12- and 1-month IPI variations.

Figure A4. Regional recession probabilities and OCDE recessions.