Figures & data

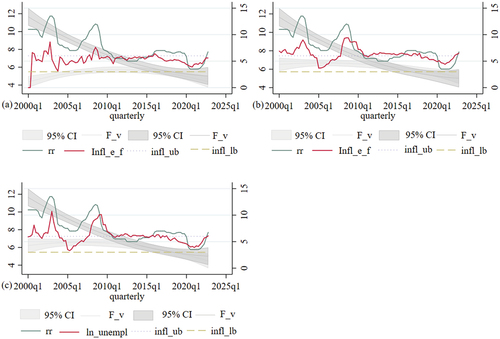

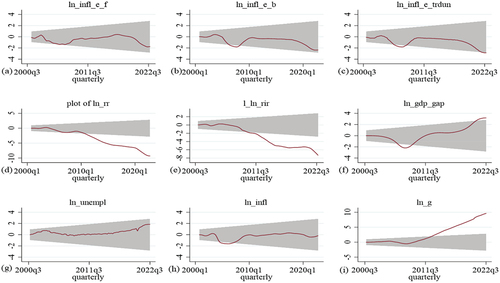

Figure 1. Economic variables of inflation expectation and the repo rate. Note the economic variables are , which is the inflation expectations for financial agents one year ahead;

, which is the inflation expectations for business agents one year ahead, and

, which is the inflation expectations for trade union agents one year ahead. On the other hand,

is a confidence interval,

is the filter value,

is the inflation upper band, and

is the inflation lower band. Composed by the authors, data sourced from (SARB, Citation2023).

Table 1. Economic variables utilised.

Table 2. Descriptive statistics.

Table 3. Matrix of correlations.

Table 4. Conventional unit root and structural break.

Table 5. Lag-order selection criteria.

Table 6. Johansen tests for cointegration.

Table 7. Long-run estimations of VEC.

Table 8. Wald tests of Granger causality for.

Table 9. Wald tests of Granger causality for and

.

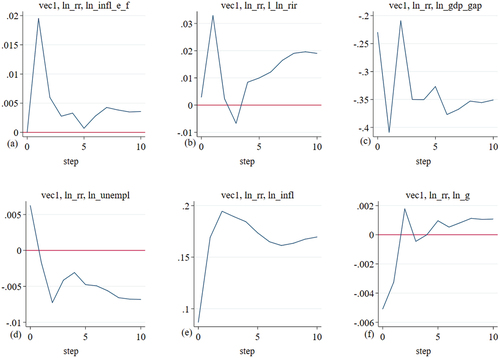

Figure 2. Shock of inflation expectations for financial agents for one year ahead on economic variables. Note that economic variables arewhich is the inflation expectations for financial agents for one year ahead,

is the repo rate,

is the lag real interest rate,

gross domestic product gap, percent change, quarterly, seasonally adjusted annual rate,

is the official unemployment rate,

is the inflation rate and is the

general government final consumption expenditure percentage of gross domestic product. Compiled by the authors.

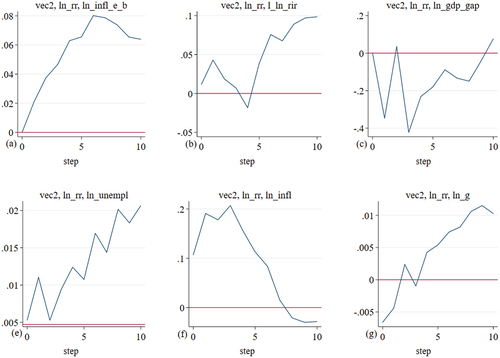

Figure 3. Shock of inflation expectations for business agents one year ahead on economic variables. Note that economic variables are , which is the inflation expectations for business agents one year ahead,

is the repo rate,

is the lag real interest rate,

gross domestic product gap, percent change, quarterly, seasonally adjusted annual rate,

is the official unemployment rate,

is the inflation rate. It is the

general government final consumption expenditure percentage of gross domestic product. Compiled by the authors.

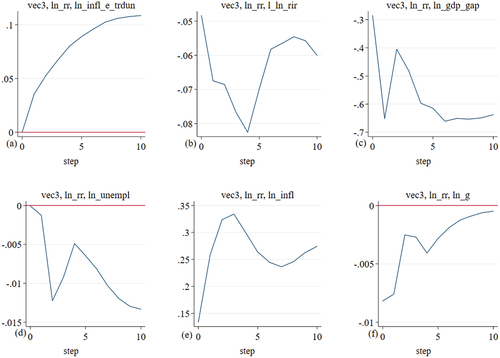

Figure 4. Shock of inflation expectations for trade union agents for one year ahead on economic variables. Note that economic variables are, which is the inflation expectations for trade union agents for one year ahead,

is the repo rate,

is the lag real interest rate,

gross domestic product gap, percent change, quarterly, seasonally adjusted annual rate,

is the official unemployment rate,

is the inflation rate and is the

general government final consumption expenditure percentage of gross domestic product. Compiled by the authors.

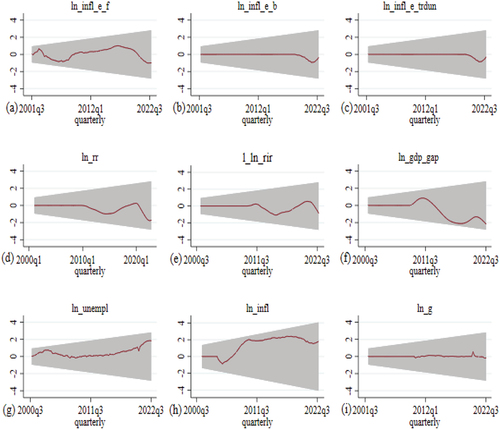

Figure A1. Period where a break in the data is considered. Note that this is with 95% confidence bands around the null. Where economic variables are , which is the inflation expectations for trade union agents one year ahead;

is the repo rate;

is the lag real interest rate;

is the gross domestic product gap, percent change, quarterly, seasonally adjusted annual rate;

is the official unemployment rate;

is the inflation rate and is the

general government final consumption expenditure percentage of gross domestic product. Compiled by the authors.

Figure A2. Period where there is no break in the data that is considered. Note that this is with 95% confidence bands around the null. Where economic variables are , which is the inflation expectations for trade union agents one year ahead;

is the repo rate;

is the lag real interest rate;

is the gross domestic product gap, percent change, quarterly, seasonally adjusted annual rate;

is the official unemployment rate;

is the inflation rate and is the

general government final consumption expenditure percentage of gross domestic product. Compiled by the authors.

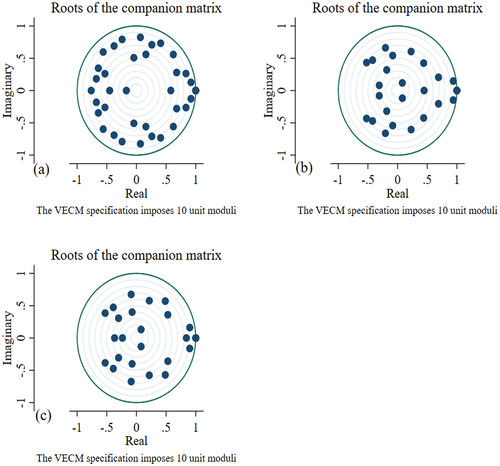

Figure A3. Stability of the ECV model estimation. Compiled by the authors.

Data availability statement

Data will be supplied upon request.