Figures & data

Table 1. The list of quantitative variables

Table 2. The list of qualitative variables

Table 3. Univariate analysis and choice of discriminant variables

Table 4. Wilks’ lambda

Table 5. The Confusion matrix

Table 6. Functions at group centroids

Table 7. The classification table

Table 8. The rating grid

Table 9. The probability of default by class

Table 10. Rating of the scoring criteria for credit portfolio managers

Table 11. Weighting of credit portfolio managers as a function of the score

Table 12. The portfolio structure in terms of default

Table 13.. () and (

) by rating class

Table 14. Non-discriminatory variables

Table 15. The quantitative and qualitative discriminating variables

Table 16. Analysis of the correlation of quantitative discriminant variables

Table 17. Results of the Box’s M test

Table 18. Wilks’ lambda

Table 19. The Confusion matrix

Table 20. The canonical correlation of variables

Table 21. The functions at group centroids

Table 22. Rating model based on linear discriminant analysis

Table 23. Explicit estimation of the probability of default by class according to experts

Table 24. Estimate of expected losses by class according to experts

Table 25. The probability of default of the experts retained for the modelling

Table 26. Bayesian rating models

Table 27. The unexpected loss according to the model

Table 28. The Bayesian unexpected loss

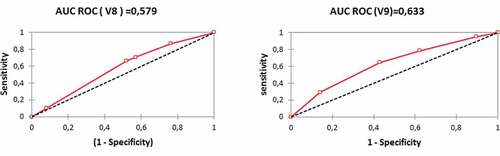

Figure 1. Comparison of the performance of correlated variables and

.

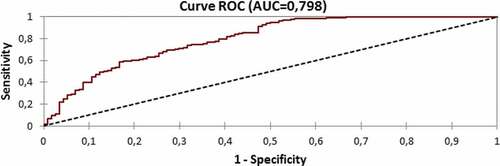

Figure 2. Performance of the linear discriminant analysis model.

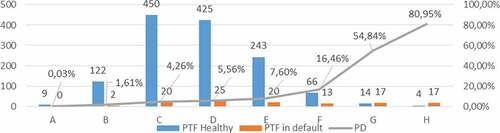

Figure 3. The distribution of healthy and defaulting enterprises and the probability of default by rating class.

Table A1. Explanation and significance of quantitative variables

Table A2. Explanation and significance of qualitative variables