Figures & data

Table 1. The descriptive statistics of variables

Figure 1. Histogram for NPL and inverse of Z-score

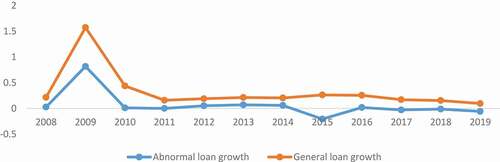

Figure 2. Abnormal and annual loan growth in the Vietnamese banking system

Note: Abnormal loan growth is defined as the difference between an individual bank’s loan growth and the median loan growth of the Vietnamese entire banking system from the same year. Meanwhile, annual loan growth is the annual growth rate of loans to customers. Both abnormal and annual loan growth are yearly averaged based on the number of banks researched.

Table 2. The correlation matrix of variables

Table 3. Baseline results for Z: Quantile regression

Table 4. Baseline results for NPL: Quantile regression

Table 5. The results of inter-quantile regression

Table 6. Baseline results for Z: quantile regression with subsample

Table 7. Baseline results for NPL: quantile regression with subsample

Table 8. Baseline results for Z and NPL: inter-quantile regression with subsample

Table 9. Abnormal loan growth and bank risk-taking, using system GMM