Figures & data

Table 1. Descriptive statistics

Table 2. Correlation analysis

Table 3. DCC-GARCH results

Table 4. AG-DCC results

Table 5. Mean differences in DCC-GARCH

Table 6. Granger causality test

Table 7. Hedging effectiveness and diversification ratio

Figure 1. Time-varying correlation of DCC-GARCH—all sample.

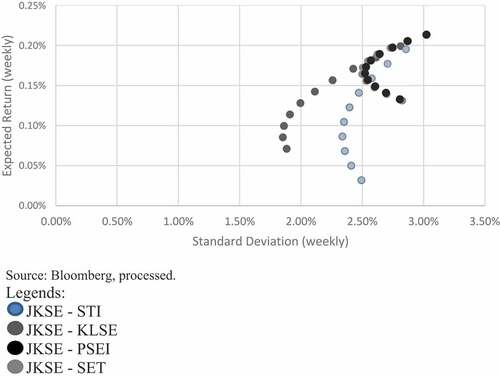

Source: Bloomberg, processed.

Figure 2. Time-varying correlation of AG-DCC—all sample.

Source: Bloomberg, processed.

Figure 3. Volatility Spillovers.

Note: the y-axis is the spillover index, the x-axis is the year, and the calculation of volatility spillovers index was done using a 200-week rolling window, a VAR lag length of 5 and 10-day-ahead forecast errors horizon (H =10).Source: Bloomberg, processed.

Table 8. Spillover Connectedness

Figure 4. Efficient Frontier.