Figures & data

Table 1. Various commodity jump models

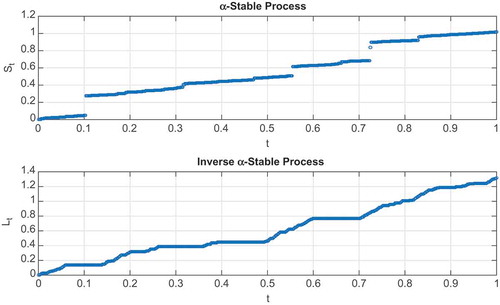

Figure 1. The top graph shows a plot of a stable process and the bottom graph shows its inverse process

simulated using exponent parameter value,

, plotted against time on the horizontal.

Figure 2. The graphs represent densities of an -stable process for different values of the exponent parameter,

. Observe the variation in the tail sizes and the skewness as the exponent parameter is varied.

![Figure 2. The graphs represent densities of an α-stable process for different values of the exponent parameter, α ∈(0,2]. Observe the variation in the tail sizes and the skewness as the exponent parameter is varied.](/cms/asset/c4141b2b-f629-46cc-a52a-d4ad0828d457/oaef_a_1512360_f0002_c.jpg)

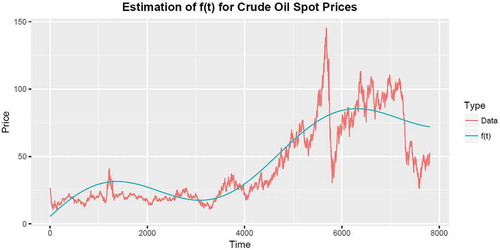

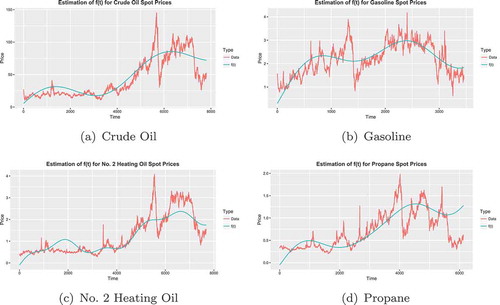

Figure 3. Seasonality is captured by the function defined in the following table. The best fit of

can be obtained by obtaining an optimal set of the

parameters.

Table 2. Estimation of parameters in the seasonality function

Table 3. Parameters obtained from maximum likelihood method

Table 4. A snapshot of the structure of the data used

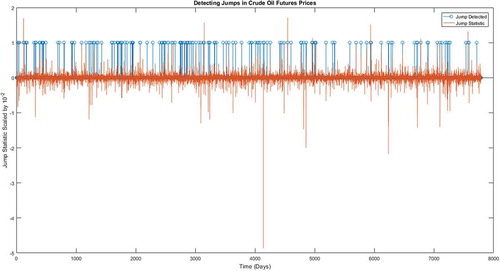

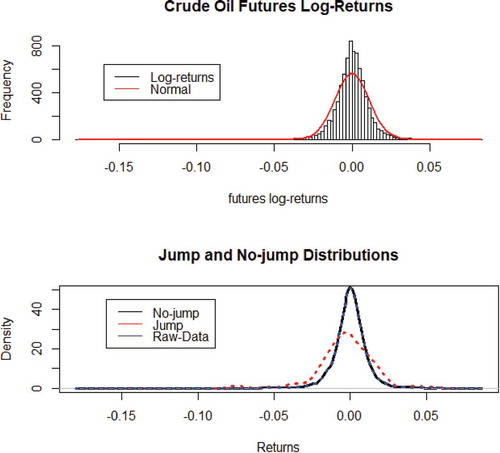

Figure 4. Detection of jumps in crude oil future prices.

Figure 5. The large spikes in the jump statistic graph reflect the extreme events in the price where as the blue strips represent the smaller jumps that might go unnoticed. The former jumps are easily detected in returns yet the latter are not that visible.