Figures & data

Table 1. Summary statistics

Table 2. Correlations

Table 3. Granger causality

Table 4. Sentiments indices versus Fama–French five factors—VAR model

Table 5. Sentiments indices versus Q-factors—VAR model

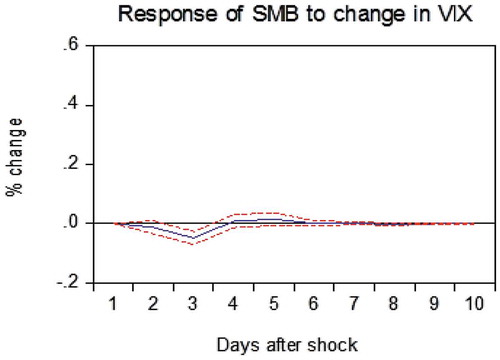

Figure 1. Impulse response function for the Fama and French (Citation2015) five-factors, Hou et al. (Citation2015) q-factors, VIX and GSVIs.

Table 6. Variance decomposition of Fama–French’s five factor, q-factors and D_VIX

Table 7. Variance Decomposition of Fama–French’s five factor, q-factors and Market Crash

Table 8. Variance decomposition of Fama–French’s five factor, q-factors and Bear Market

Table 9. Variance decomposition of Fama–French’s five factor, q-factors and Bull Market

Table 10. Variance Decomposition of Fama–French’s five factor, q-factors and Market Rally

Table A1. Monday effects in Fama and French’s RMW factor.