Figures & data

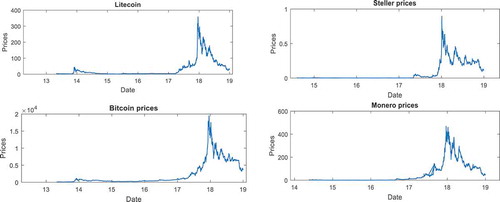

Figure 1. Prices of Cryptocurrencies

Table 1. Summary statistics of cryptocurrencies returns

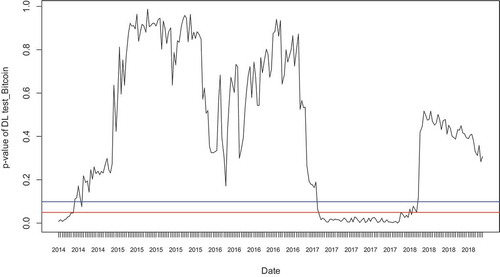

Figure 2. P-values of Dominguez-Lobato test of Bitcoin

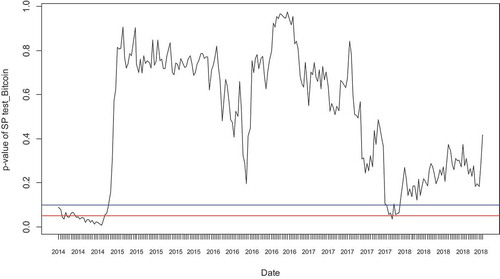

Figure 3. P-value of Generalized Spectral Test of Bitcoin

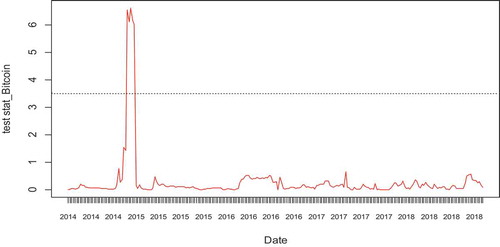

Figure 4. Stats of Automatic Portmanteau Test of Bitcoin

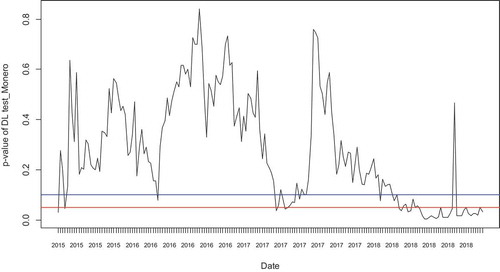

Figure 5. P-values of Dominguez-Lobato Test of Monero

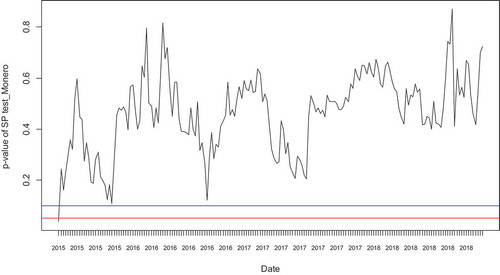

Figure 6. P-values of Generalized Spectral test of Monero

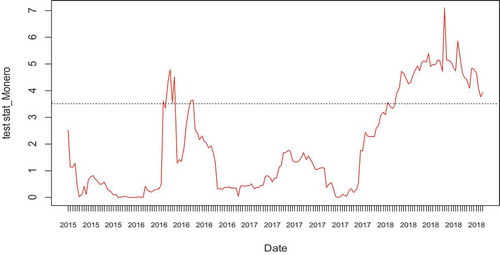

Figure 7. Stats of Automatic Portmanteau Test of Monero

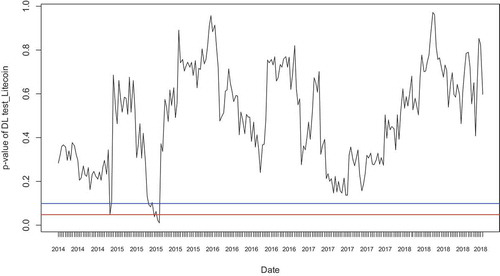

Figure 8. P-values of Dominguez-Lobato test of Litecoin

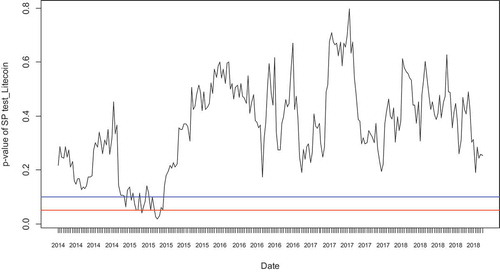

Figure 9. P-value of Generalized Spectral Test of Litecoin

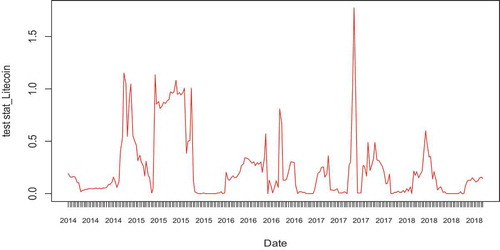

Figure 10. Stats of Automatic Portmanteau Test of Litecoin

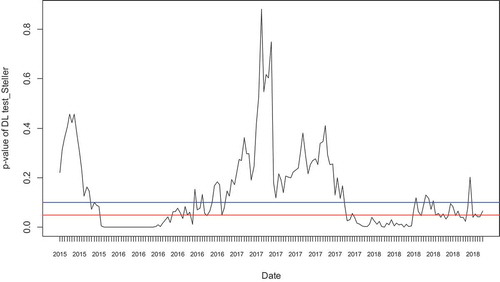

Figure 11. P-values of Dominguez–Lobato Test of Steller

Figure 12. P-values of Generalized Spectral Test

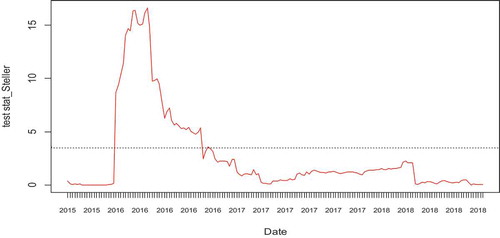

Figure 13. Stats of Automatic Portmanteau Test of Steller