Figures & data

Table 1. The information about the independent and dependent variables used in the analysis are given below

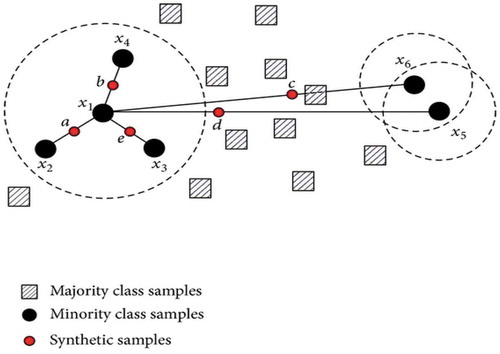

Figure 1. SMOTE algorithm (Synthetic data generation method)

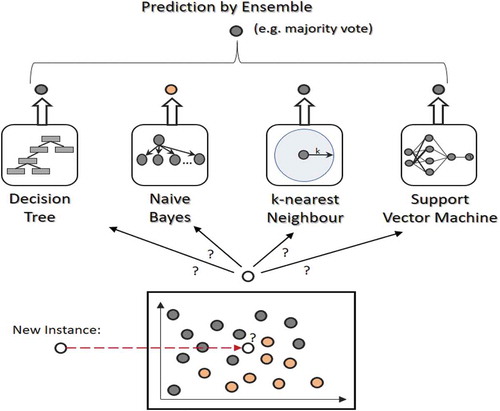

Figure 2. Ensemble learning method

Figure 3. Bagging procedure for algorithm learning

Table 2. Descriptive statistics for private and public sector Indian banks for the period of 2000–2017

Table 3. Preliminary data analysis the Table 3 describes the descriptive statistics of accounting profiles to survived vs. Failed banks. The t-tests on the mean difference for different classifications of banks are given below

Table 4. Confusion matrix—Actual values vs predicted results

Table 5. Actual vs predicted—logistic regression

Table 6. Actual vs predicted—random forest method

Table 7. Actual vs predicted—AdaBoost method

Table 8. Accuracy and Type-II error of the different algorithms on the test data