Figures & data

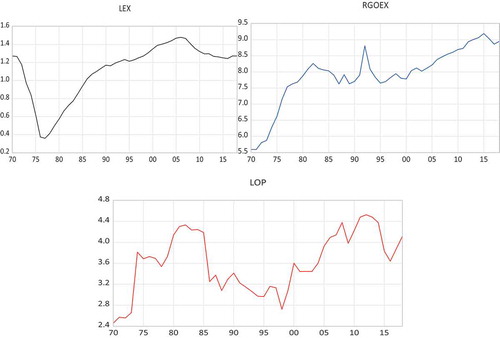

Figure 1. Log real exchange rate, real government expenditure, and real OPEC basket oil price.

Table 1. Results of descriptive statistics of government expenditure (GOEX), oil prices (OP), and real exchange rate (EX) for the period of 1970–2018

Table 2. Augmented-Dickey Fuller and Phillips-Perron tests

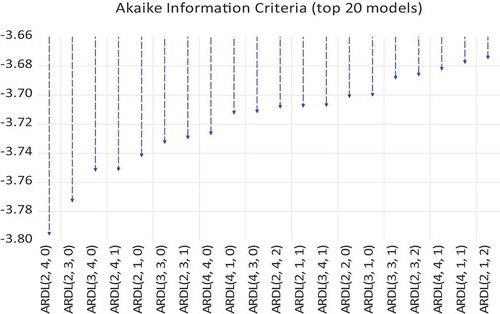

Figure 2. The strength of model selection criteria.

Table 3. VAR lag order selection criteria

Table 4. The ARDL regression with dependent variable LEX

Table 5. FMOLS estimates with dependent variable LEX

Table 6. The ARDL error correction dependent variable LEX

Table 7. Long-run estimates with dependent variable LEX

Table 8. Serial correlation LM test

Table 9. F-bBounds test

Table 10. Heteroskedasticity test

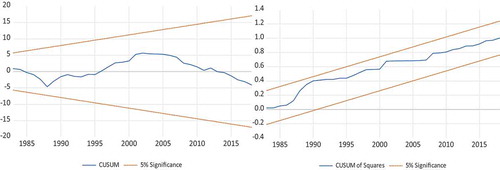

Figure 3. Stability test of the model.

Table 11. Variance decomposition

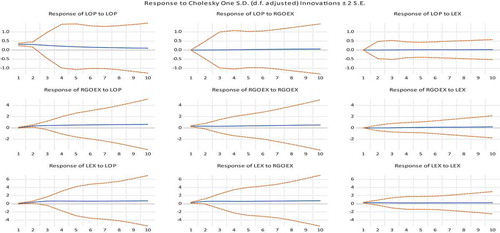

Figure 4. Responses of RGOEXt, LEXt to symmetric oil price shocks LOPt.