Figures & data

Table 1. Descriptive statistics results

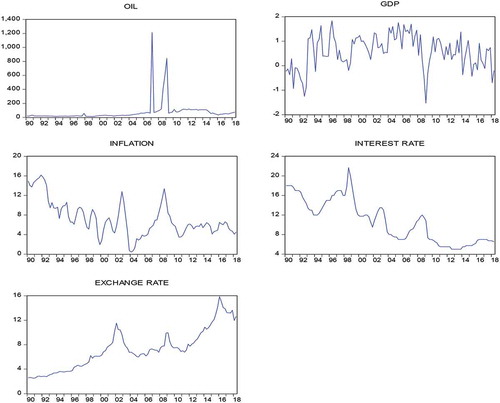

Figure 1. Time series plots at level.

Table 2. Stationarity test results

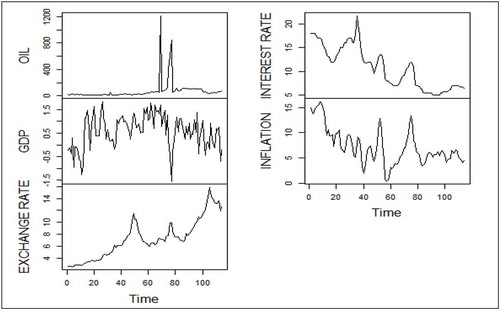

Figure 2. Residual time series plots.

Table 3. Parameter estimation results of the ARCH model

Table 4. Parameter estimation results of the GARCH and EGARCH model

Table 5. Diagnostic test results