Figures & data

Table 1. Copula functions and its characteristics

Table 2. Copula Parameters

Table 3. Descriptive Statistics of Returns of Daily Stocks and World Crude Oil

Figure 1. Normal q-q plots of returns of stock indices for period 1.

Figure 2. Normal q-q plots of returns of stock indices for period 2.

Figure 3. Normal q-q plots of returns of stock indices for period 3.

Table 4. Dependence coefficient of WCOR and SR in pre-depression period

Table 5. Dependence coefficient of WCOR and SR in depression period

Table 6. Dependence coefficient of WCOR and SR in post- depression period

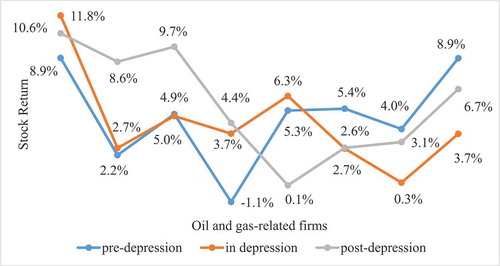

Figure 4. DCs between WCOR and SR in three periods.

Table 7. Estimation of copula parameters for WCOR and PVD in pre-depression period and best copula

Table 8. Estimation of copula parameters for WCOR and PVD in depression period and best copula

Table 9. Estimation of copula parameters for WCOR and PVD in post- depression period and best copula

Table 10. The choice of the best copula for WCOR and Vietnam’s oil and gas stock returns, and tail dependence coefficients in each period

Table 11. Granger Causality Test