Figures & data

Table 1. Descriptive statistics of the IIR

Table 2. ARMA model to the IIR

Table 3. The conditional mean and variance models for the Investment industry

Table 4. The conditional mean and variance models for the Investment industry under MRS method

Table 5. Conditional mean and variance model of IIRs without the ARCH effect under MRS

Table 6. The results of likelihood ratio for GARCH family models

Table 7. The results of the likelihood ratio for the MRS- GARCH family models

Table 8. The optimal model of industries that have the ARCH effect

Table 9. The optimal model of the IIR

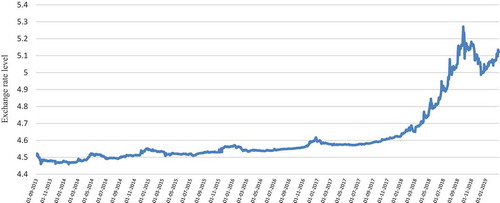

Figure 1. The logarithm of the USD/IRR rate from 1 September 2013 to 27 February 2019.

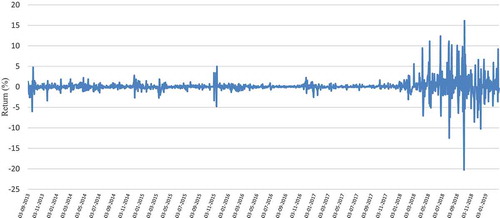

Figure 2. The USD/IRR rate daily returns from 1 September 2013 to 27 February 2019.

Table 10. Short-term and long-term effect of the exchange rate on the IIR uncertainty

Table

Table

Table

Table

Table

Table

Table

Table

Table

Table