Figures & data

Table 1. Summary of descriptive statistics

Table 2. Philip-Perron unit root test at level

Table 3. Philip-Perron unit root test at 1st difference

Table 4. VAR model optimal lag lengths check

Table 5. Granger causality Wald test result for the base model

Table 7. Variance decomposition of base model [ordering reflects Cholesky ordering]

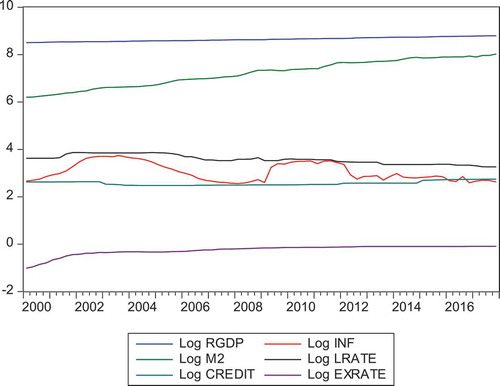

Figure 1. Graphs of Variables from Ghana Money Market in Log Levels

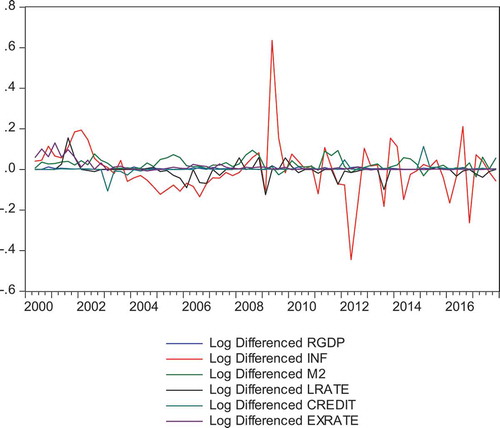

Figure 2. Graphs of Differenced Series of Variables in the Ghanaian Money Market

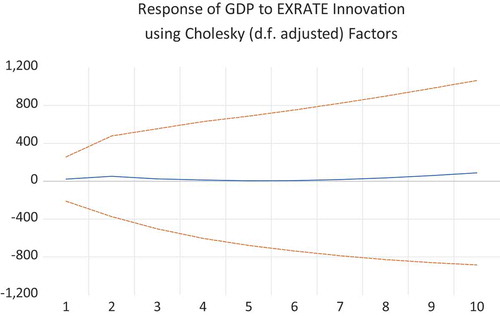

Figure 3. Responses of Real GDP to Exchange Rate

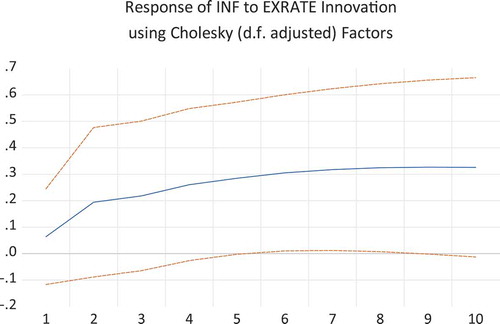

Figure 4. Responses of Inflation to Exchange Rate

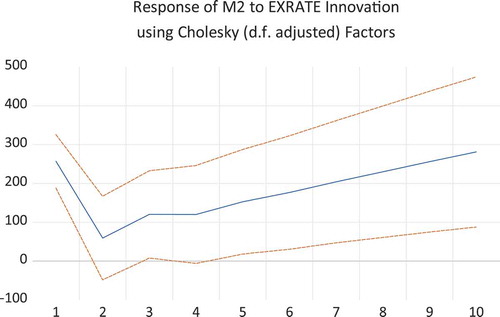

Figure 5. Responses of Money Supply to Exchange Rate

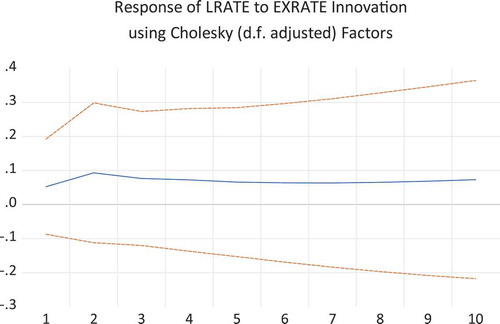

Figure 6. Responses of Lending Rate to Exchange Rate

Table A1. Optimal lag length checks for the Basic VAR Model for Ghana

Table A2. VAR Residual correlation LM TEST

Table A3. VAR Residual Portmanteau Test for Autocorrelations

Table A4. VAR Residual Heteroskedasticity Test for the Base VAR Model

Table A5. VAR Residual Normality Test for Skewness

Table A6. VAR Residual Normality Test for Kurtosis

Table A7. VAR Residual Normality Test for Jarque-Bera

Table A8. VAR Lag Exclusion Wald Tests Chi-squared test statistics for lag exclusion: Numbers in () are p values

Table A9. Regression Result for the Base VAR Model for Ghana Standard Errors in () and t-Statistics []