Figures & data

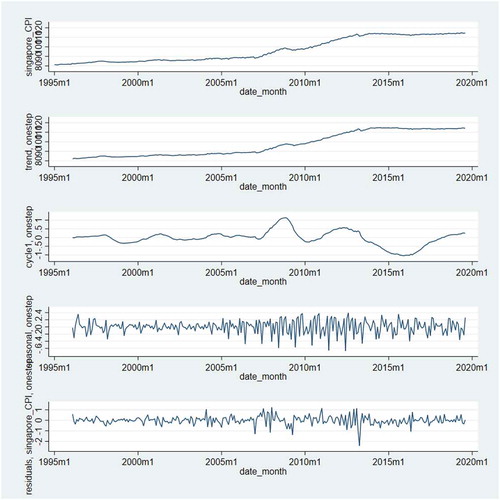

Figure 1. The application of UCM in adjusting Singapore CPI

Table 1. Hurst’s exponents

Table 2. Descriptive statistics

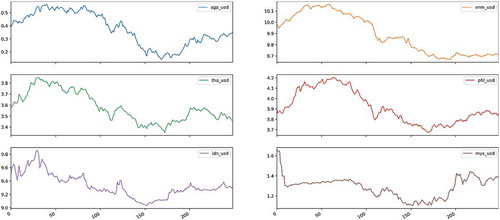

Figure 2. Real exchange rate

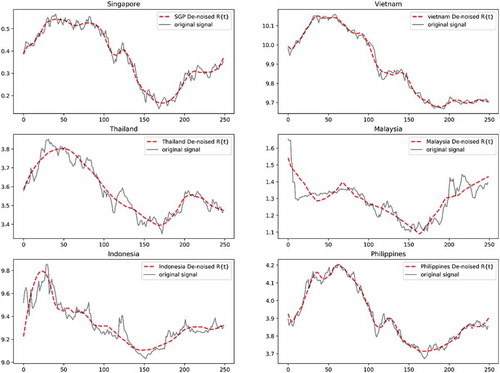

Figure 3. De-noised real exchange rate

Table 3. Univariate stationary test results

Table 4. Panel stationary test results

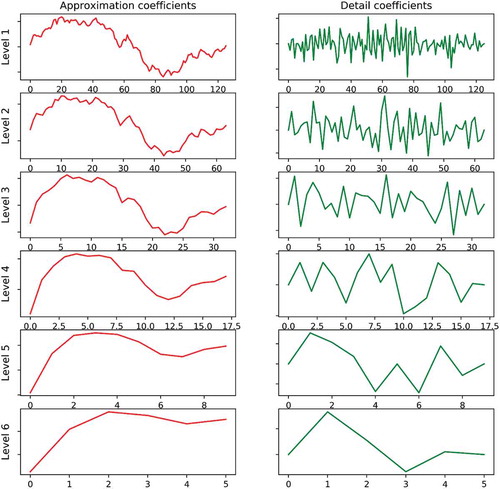

Figure 4. Multi-level decomposition of SGP/USD real exchange rate

Table 5. Insights of the MRA mechanism

Table 6. Univariate stationary test results on six real exchange rate—Averaging coefficients

Table 7. Univariate stationary test results on six real exchange rate detailed coefficients

Table 8. The multivariate test results on six averaging coefficients and detailed coefficients

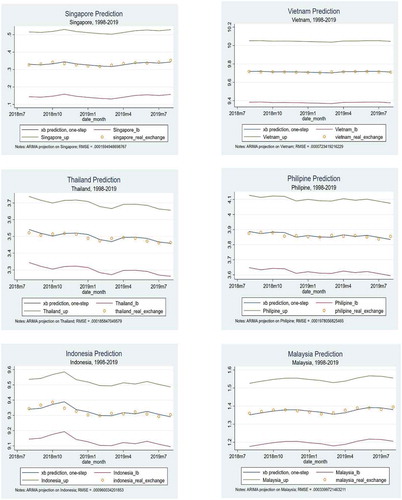

Figure 5. ARIMA on six real exchange rate series

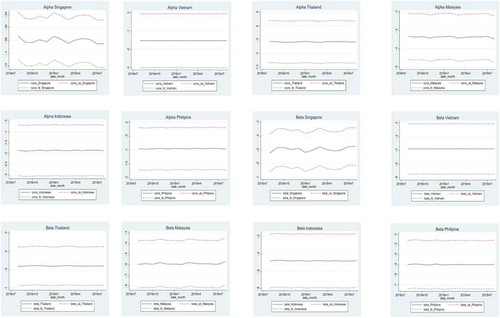

Figure 6. The estimated alpha and beta coefficients