Figures & data

Table 1. Idiosyncratic Volatility and Stock Returns

Table 2. Capital gains overhang in the relation between IVOL and future returns

Table 3. Cross-sectional test within Idiosyncratic Risk

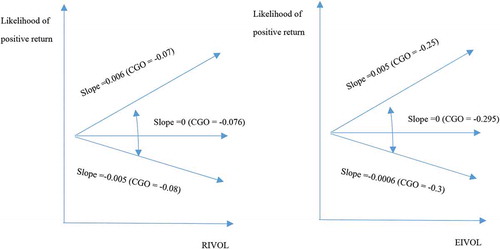

Figure 1. Relationship between IVOL and likelihood of positive for various levels of CGO

Table 4. Time series regressions within Idiosyncratic Risk