Figures & data

Table 1. VAR model estimates for the market of ETFs with domestic benchmarks

Table 2. VAR model estimates for the market of ETFs with international benchmarks

Figure 1. Impulse response functions for the VAR model estimated for the market of ETFs with domestic benchmarks

Notes:The blue line represents the impulse response and the red lines represent two standard error bands.

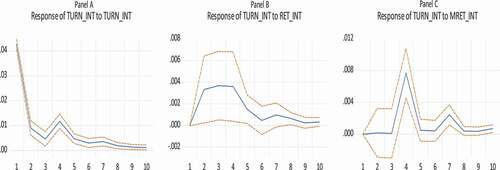

Figure 2. Impulse response functions for the VAR model estimated for the market of ETFs with international benchmarks

Notes:The blue line represents the impulse response and the red lines represent two standard error bands.

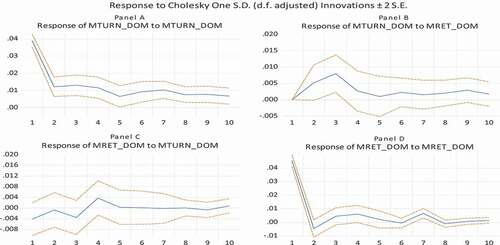

Table 3. Panel VAR model estimates for ETFs with domestic benchmarks

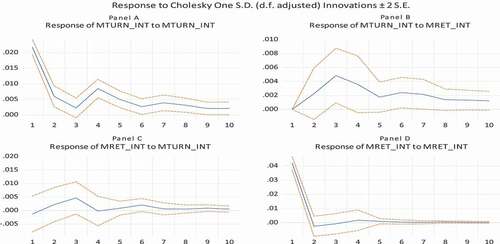

Table 4. Panel VAR model estimates for ETFs with international benchmarks

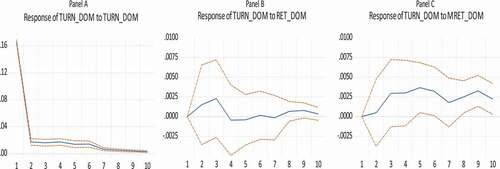

Figure 3. Impulse response functions for ETFs tracking domestic benchmarks

Notes:The blue line represents the impulse response and the red lines represent two standard error bands.

Figure 4. Impulse response functions for ETFs tracking international benchmarks

Notes:The blue line represents the impulse response and the red lines represent two standard error bands.