Figures & data

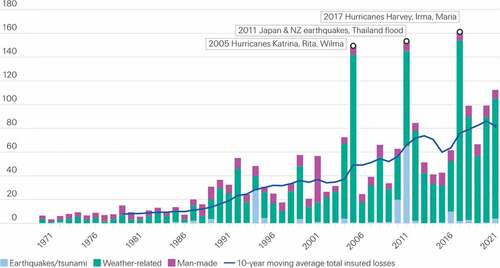

Figure 1. Insured losses since 1970 (USD billion in 2021 prices). Source: .swiss Re Institute (Citation2021)

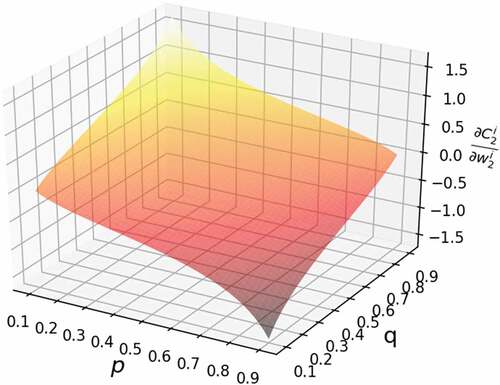

Figure 2. Three dimensional plot of the ratios of premium loading factor to the loss probability.

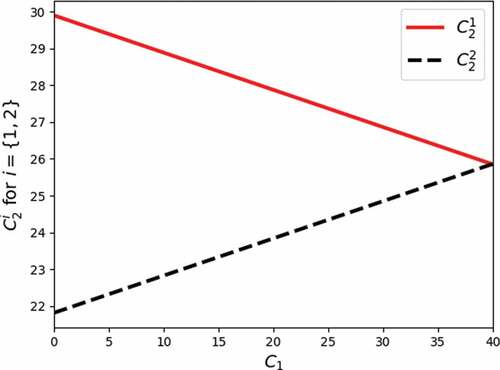

Figure 3. Comparison of loss () and no loss (

) against

.

Table 1. Nominal values of the parameter

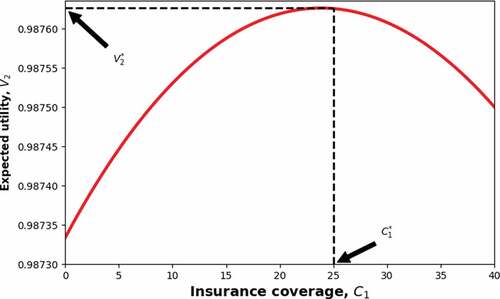

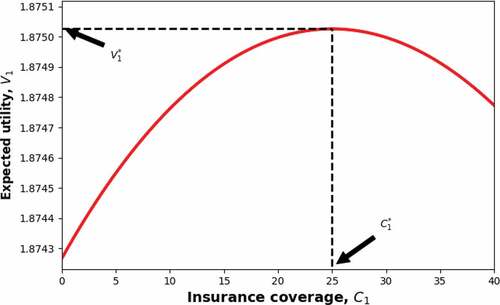

Figure 4. Optimal insurance coverage with intertemporal consideration. The optimal value is at , at which point the greatest expected utility is valued at

. (The interval of

over which the plotting is done was subdivided

times to ensure that an accurate value of the index of

is used to obtain the maximum value of

).

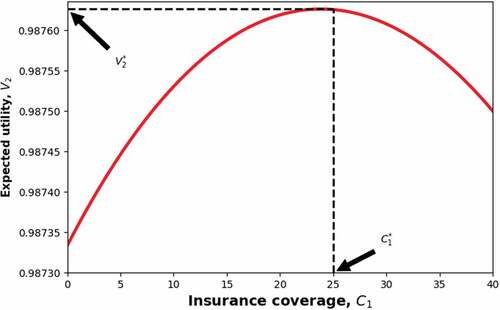

Figure 5. Optimal insurance coverage with intertemporal consideration. The optimal value is at , at which point the greatest expected utility is valued at

.