Figures & data

Table 1. Descriptive statistics

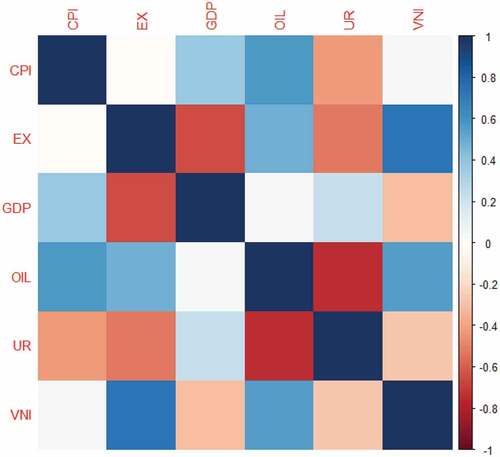

Figure 1. Pearson correlation matrix for OIL, EX, CPI, UR, GDP and VNI in Vietnam.

Notes: the color bar represents the magnitude of the intensity for correlation between indicators.

Table 2. Quantile autoregression unit root analysis

Table 3. Quantile cointegration test

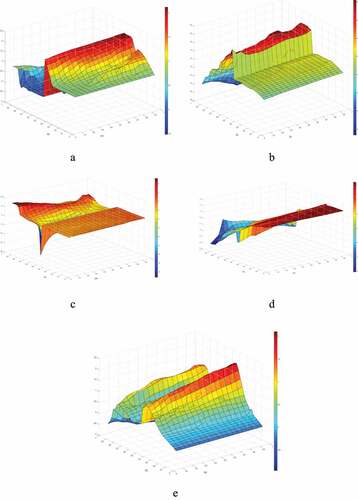

Figure 2. (a) The impact of oil prices on inflation. (b) The impact of oil prices on exchange rate. (c) The impact of oil prices on economic growth. (d) The impact of oil prices on unemployment rate. (e) The impact of oil prices on stock market prices.

Table 4. Granger causality in quantile test results

Table 5. QRA estimates of oil prices and other indicators

Data availability statement

Please contact author for data and program codes requests. R and Matlab are used to organize data.