Figures & data

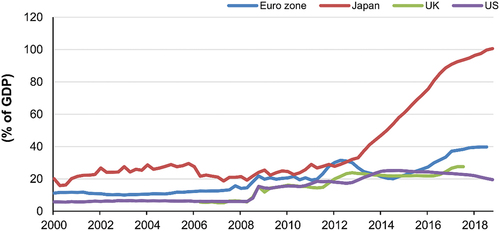

Figure 1. Central bank assets as a percentage of nominal gross domestic product.

Table 1. Summary statistics for the BoJ’s ETF purchases

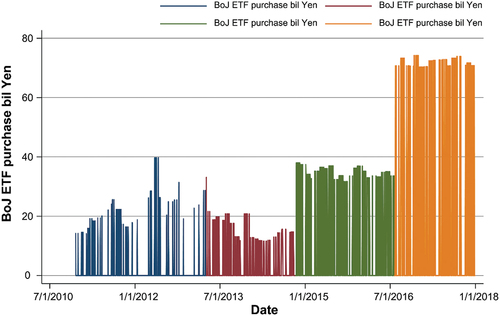

Figure 2. The BoJ’s exchange-traded fund (ETF) purchasing volume over time, 2010–2018.

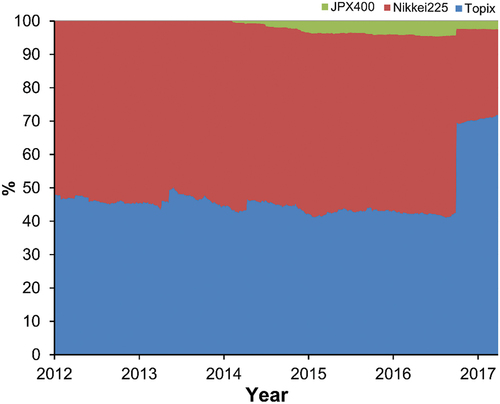

Figure 3. Composition of the BoJ’s ETF purchases, 2012–2017.

Table 2. Descriptive statistics based on the BoJ’s ETF purchases

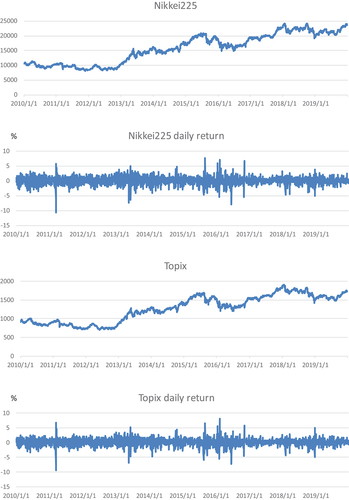

Figure 4. Historical charts for the Nikkei225, Topix, S&P500, and USD/JPY, 2010–2019.

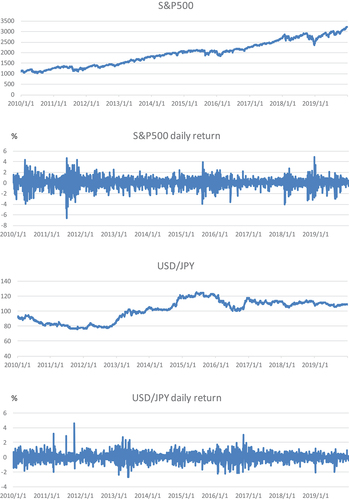

Figure 4. Continued.

Table 3. Estimation results of simple OLS regression EquationEquation (1)(1)

(1)

Table 4. Estimation probit model results EquationEquation (2)(2)

(2)

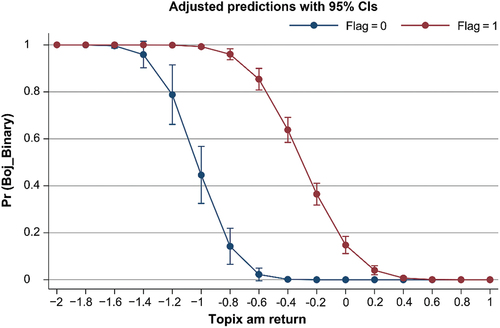

Figure 5. Estimated probability of the BoJ’s ETF purchases using the probit model.

Table 5. Predictive power of the probit model

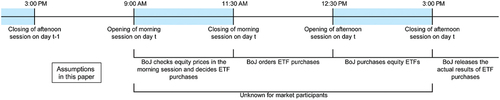

Figure 6. Assumed timeframe for the BoJ’s ETF purchasing operation.

Table 6. OLS regression results for afternoon returns Equation (3)

Table 7. Impact of expected and unexpected ETF purchases by the BoJ EquationEquation (4)(4)

(4)

Table 8. OLS regression results for returns reversals EquationEquation (5)(5)

(5)

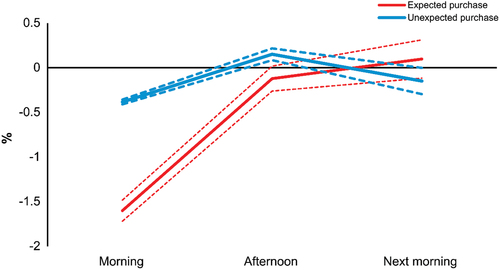

Figure 7. Topix returns when the BoJ purchases ETFs.