Figures & data

Table 1. Variable description and source of data

Table 2. Descriptive statistics of variables in the model

Table 3. ADF unit root test results

Table 4. Testing optimal lag selection of PVAR model for Asia

Table 5. Testing optimal lag selection of PVAR model for Europe

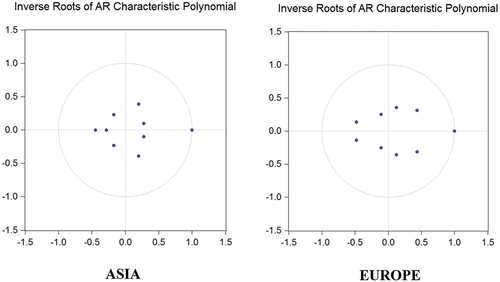

Figure 1. Inverse roots of AR characteristic polynomial.

Table 6. Results of Granger causality test

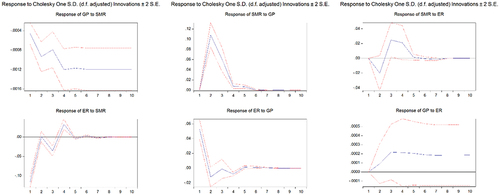

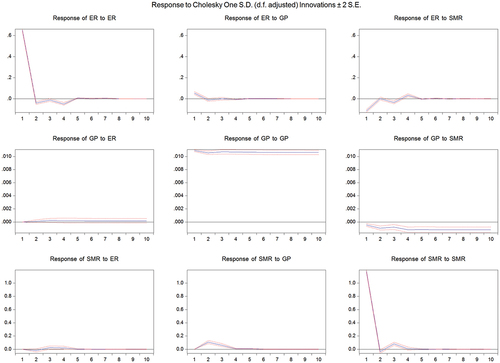

Figure 2. Impulse-response function in Asia.

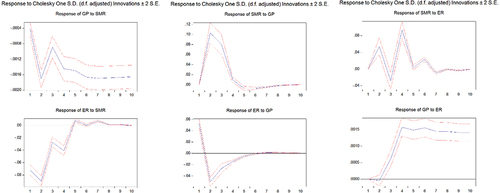

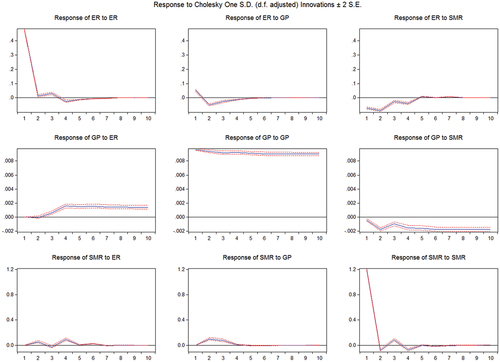

Figure 3. Impulse-response function in Europe.

Table 7. Variance decomposition analysis

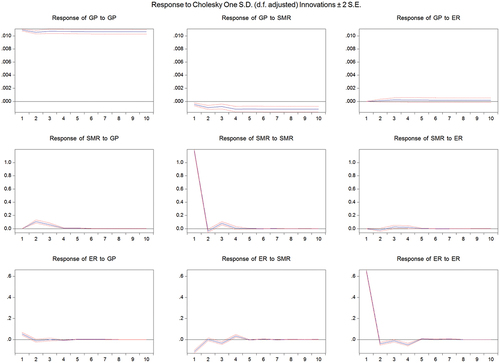

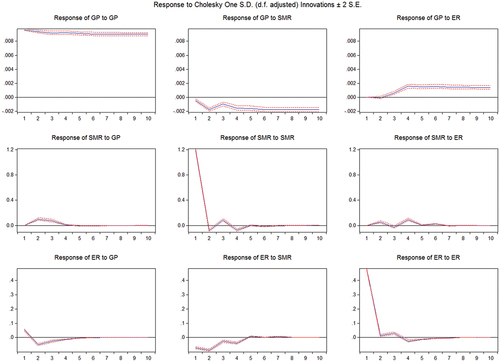

Figure 4. Ordering of Asian countries’ PVAR: GP, SMR, ER.

Figure 5. Ordering of Asian countries’ PVAR: ER, GP, SMR.

Figure 6. Ordering of European countries’ PVAR: GP, SMR, ER.

Figure 7. Ordering of European countries’ PVAR: ER, GP, SMR.

Table A1. Review of selected studies on the relationship between stock market, gold price and exchange rate