Figures & data

Table 1. Unit root tests

Table 2. Descriptive statistics

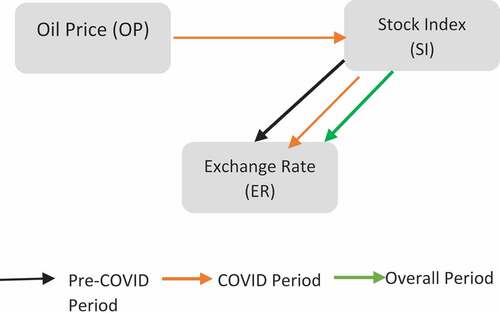

Figure 1. VAR Granger Causality Test. Source: Author’s own.

Table 3. Wald Joint Sig. Test

Table 4. Unrestricted VAR

Table 5. Unrestricted VAR

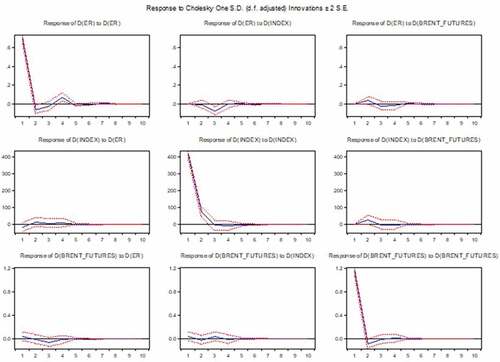

Figure 2. Impulse-Response-Function pre-COVID period. Source: Author’s own.

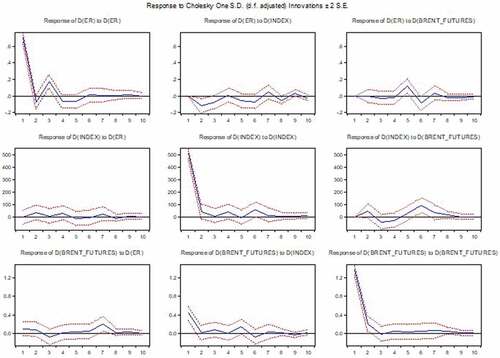

Figure 3. Impulse-Response-Function during COVID period. Source: Author’s own.

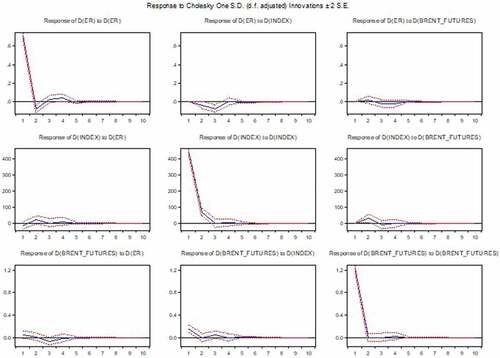

Figure 4. Impulse-Response-Function in overall period. Source: Author’s own.

Table 6. Variance Decompositions (VDCs)—pre-COVID period

Table 7. Variance Decompositions (VDCs)—during COVID period