Figures & data

Table 1. Descriptive statistics

Table 2. Coefficient of Variation (CoV)

Table 3. Augmented dickey fuller (ADF) unit root test for three regimes

Table 4. Philips peron unit root test for three regimes

Table 5. KPSS unit root test for three regimes

Table 6. Zivot Andrew (ZA) Unit root test for three regimes

Table 7. Optimal Lag length criteria

Table 8. Unrestricted Co-Integration Rank test (Trace)

Table 9. Unrestricted Vector Auto regression modelling results: Dependent variable: Stock Indexes

Table 10. Unrestricted Vector Auto regression modelling results: Dependent variable: Exchange rate

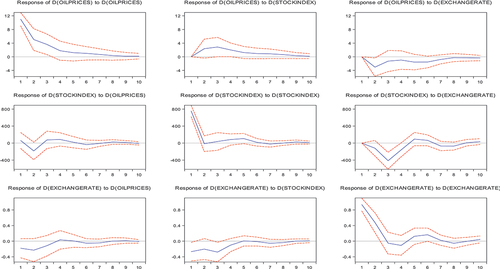

Figure 1. Impulse response function for pre-crisis period.

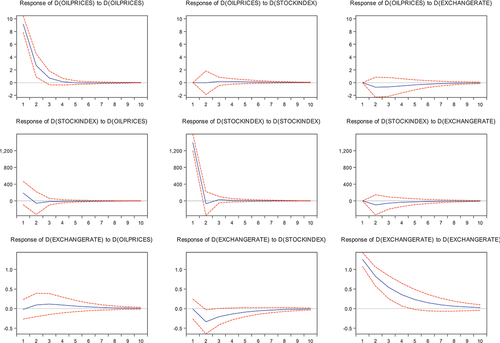

Figure 2. Impulse response function after crisis.

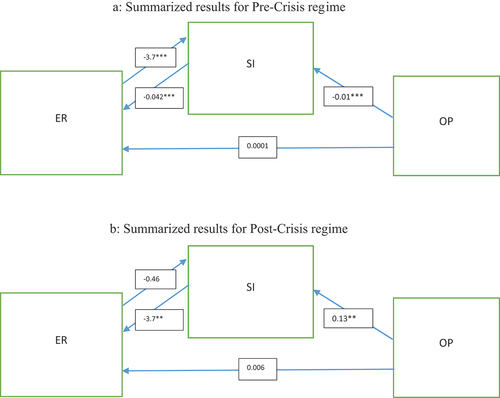

Figure 3. Mediating role of stock market indices between exchange rate and oil price retunes. a) Summarized results for Pre-Crisis regime, b) Summarized results for Post-Crisis regime.